|

|

| |

|

March 2019

|

What does Budget 2019 mean for you?

|

The following proposed tax changes were announced

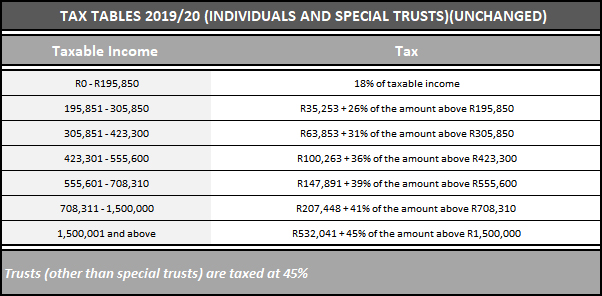

- Income tax rates are left unchanged. The primary rebate was marginally increased but the overall effect of this is that individuals will pay R12.8 billion more in tax – the so called “bracket creep” which means you pay higher taxes as salary increases will put you into higher tax brackets.

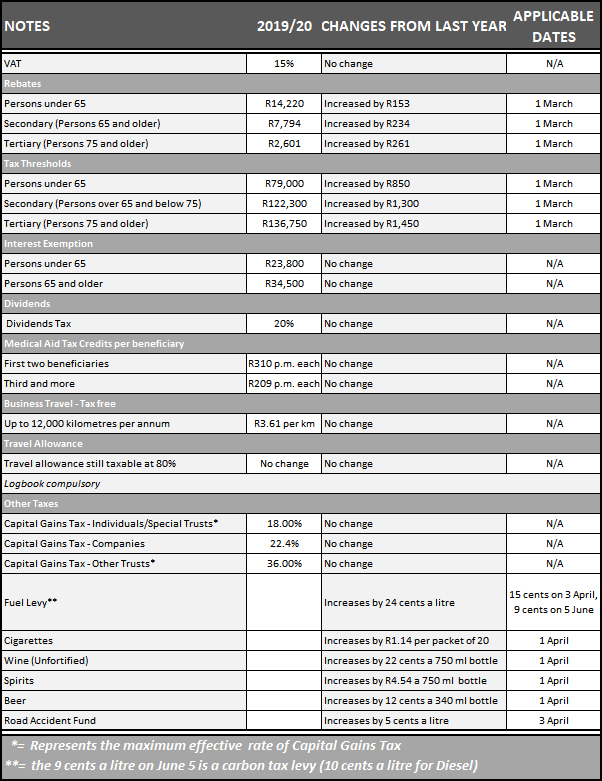

- “Sin” taxes have all been increased with beer, wine, spirits and cigarettes going up on 1 April (see tables below). Indirect taxes will bring R2.3 billion into the fiscus in the 2019/20 tax year.

- The Sugar Tax will be increased to 2.21cents per gram up from 2.1 cents per gram.

- The new Carbon Tax will come into effect on 1 June this year – originally intended for 1 January but only passed in Parliament in February. The tax will have a three year phase-in and is primarily intended to fulfil South Africa’s pledge to reduce carbon emissions by 50% by 2030. It will mean substantial administration in affected industries such as engineering.

- A carbon levy will go into effect on 5 June and will be charged on the fuel price at 9 cents per litre.

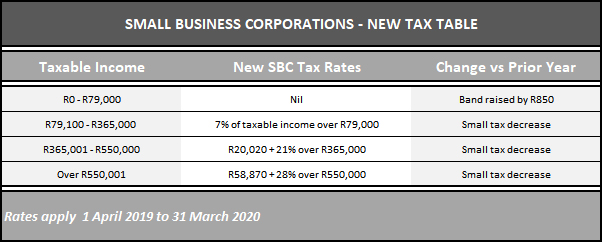

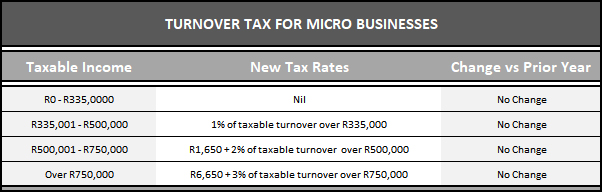

- Micro Business Turnover Tax. There is a marginal decrease in the Small Business Corporation Tax.

The following taxes are unchanged

- Dividend tax at 20%

- Retirement savings contribution limit remains at 27.5% of income

- Capital Gains Tax at 18% for individuals, 22.4% for companies and 36% for trusts

- Company Tax at 28% and Trusts at 45%

- Transfer Duties, Tyre Levies, Plastic Bag Levy, Incandescent Light Levy and other Environment Levies

- All withholding taxes

- The Interest Exemption on Income Tax - R23,800 if you are under 65 and over 65 R34,800

- There is no change to the Medical Tax Credit as the country begins to phase in National Health Insurance.

Tables - Tax Changes Budget 2019

|

|

Your Selection of Budget 2019 Tax Calculators

|

“People who complain about taxes can be divided into two classes: men and women” (Anon)

- How long will you work for the taxman today?

Input your salary into the 2019 Tax Clock calculator and find out how many hours you will spend today working for the taxman, and at what time precisely you will finally start working for yourself (warning – it’s not pretty!).

- How will your income tax change?

Put your monthly taxable income into Fin24’s Budget 2019 Income Tax Calculator to find out.

- How much extra will your sin taxes cost you this year?

Work out how much more you will be shelling out for spirits, wine, beer and cigarettes (or how much you will be saving if you don’t indulge!) with Fin24’s Budget 2019 Sin Tax Calculator.

|

|

Budget 2019: Credibility Restored?

|

“It is not the critic who counts; not the man who points out how the strong man stumbles, or where the doer of deeds could have done them better. The credit belongs to the man who is actually in the arena, whose face is marred by dust and sweat and blood; who strives valiantly; who errs … but who does actually strive to do the deeds…” (Theodore Roosevelt 1910)

One of the shining lights of the country was the ability of Treasury to maintain fiscal discipline and not overburden the government with unmanageable debt. Since 2015, debt has risen quickly whilst tax revenues have slowed – debt to GDP (Gross Domestic Product) was 2.5% in 2015 but is now over 4% whilst tax collections will miss their 2018/19 target by R50 billion. Government debt to GDP was just over 40% in 2015 but is 56% now and is forecast to go above 60%.

All of these are alarming ratios but this was an unusual budget with the Eskom crisis the primary focus – the State-Owned Enterprise (SOE) only has sufficient funds to stay in business until April, has R420 billion in debt (R292 billion guaranteed by government) and cannot generate enough revenue to service this debt. The problem for government is that if Eskom collapses, then the economy basically stops – in the words of the President, Eskom is too big to fail. Yet its rescue is being closely watched by Moody’s – the only ratings agency not to rate South Africa's debt as junk. Should Moody’s reduce us to junk status (and although they are scheduled to assess SA’s debt on 29 March they are expected to announce their decision after the May election) then off-shore institutions will be forced to sell R140 billion of government debt. This will have severe knock on effects, tipping our economy back into recession with a falling currency followed by interest rate hikes.

It is in this light that the Budget of Minister Mboweni should be judged.

In essence, the Budget is a holding operation in terms of tax changes as moves are made to deal with the Eskom crisis. The deficit to GDP will be 4.2% this year and will rise to 4.5% next year before declining in the out-years. Borrowing as a percentage of GDP will now breach 60% in 2024.

GDP will grow at 1.7% this year rising to 2.1% in three years. Inflation will rise from 4.7% now to 5.4% in 2022.

Government has taken R50 billion in cost cuts from the Medium Term three year budget – the main reduction is in government salaries with early retirement being offered to senior civil servants. Based on the assumption that 30,000 employees will take this up, the saving will be over R20 billion. The Minister emphasised that the government salary bill is unsustainable at 35% of government expenditure. Cuts were also made to overtime allowances, the government bonus scheme will be phased out and there is a salary freeze on senior SOE staff and cabinet and members of parliament.

Despite these savings the debt ceiling (a holy cow for Ratings Agencies) will be breached by R16 billion before coming back to within the ceiling.

Even before considering Eskom, these are sobering figures and the fact that the Minister laid them out starkly in an election year shows how the country cannot keep deferring the urgent issues it faces.

Eskom

The President had already announced the intended split up of Eskom into three units: generation, distribution and transmission. This would allow greater management focus on the discrete parts of Eskom. The Minister said that R23 billion will be set aside for each of the next three years to assist the SOE with its reorganisation into the three units and to help with its debt service costs.

Eskom will need to save R20 billion in costs per annum over this period. Although Minister Mboweni only gave a three year outlook, the restructuring of the SOE will clearly be a long term effort and government will need to be committed for as long as it takes.

In order for Eskom to access the R23 billion, it will need to get the approval of a Chief Restructuring Officer (CRO) who will be appointed by Ministers Pravin Gordhan and Tito Mboweni. The CRO will operate within restructuring requirements to be announced by the President in the next few weeks. The CRO will be the eyes and ears of the government.

Other SOEs will need to appoint a CRO if they wish to access government funds – R6 billion has been provided in the Contingency Reserve for this.

It is as if the recent loadshedding has brought a new urgency in tackling the sizeable problems that Eskom and other SOEs present. What is refreshing about the approach taken by Minister Mboweni is that he and the President are breaking the mould of government thinking – the fact that the Minister openly questioned the rationale for many of these SOEs and called for breaking away from old Soviet paradigms shows we are moving into a new era.

Will this be successful?

There are enormous risks ahead, not least of which is the Moody’s rating decision. Moody’s are looking for a new credible approach to tackling Eskom and this is being laid out by the government. Trade Unions are already mobilising to fight the Budget and the reforms at Eskom. Perhaps the most encouraging aspect is that both Minister Tito Mboweni and President Ramaphosa seem up for the challenge.

If you strip Eskom out of the next three years, then there would be no breach of the debt ceiling and the debt to GDP ratio would not go above 60%. In fact the fiscal consolidation that Treasury has been desperately trying to instil since 2015 would be credible as the 2019 Budget would be in line with the projection of last year’s Budget.

|

|

How to Improve Risk Management in Your Business

|

Risk management has become increasingly popular in the past twenty years. It is also a corner stone of good governance.

Despite this increased focus, businesses are still being blindsided by events which result in high costs being incurred.

Potential problems and unpredictability – think “out of the box”

Usually a risk assessment is done via a matrix and once all known risks have been identified, they are ranked in terms of cost to the business should they occur.

That’s a limited way of doing this process as recent events have shown just how unpredictable the world is getting, for example a volcano in Iceland shutting down most flights into Europe.

Don’t just think of risks you know about but think of some potential event that could close down your business for an indefinite period. Even if you can’t envisage something specific that could shut you down, you can prepare for such an eventuality.

Optimistic versus pessimistic

Most of us are optimistic when we look into the future and thus we tend to be optimistic when doing a risk matrix. The business would be better served if a more pessimistic or a more even-handed, realistic approach was taken.

Consider operational risks also

Most risk assessments tend to happen at a high level, such as “is our sales strategy sound with risks catered for?” But do we think of what can go wrong operationally? The BP disaster in the 2010 Gulf of Mexico highlights this issue – a maintenance failure led to an explosion which killed 11 people, led to 3 million barrels of oil leaking into the sea and caused the BP share price to fall 50%.

Why not include risk mitigation in job descriptions of middle and lower middle management in your organisation with an emphasis placed on operational risk?

Risk is a dynamic process – keep thinking of what can go wrong and of how to minimise the chance of it happening.

|

|

VAT Taxpayers: New Relief on Correcting Tax Invoices

|

There has been an anomaly in VAT law which new legislation has now largely resolved.

The problem with the old position

It has always been simple to correct calculable errors in tax invoices, such as price. A VAT debit or credit note would fix such mistakes. However, other errors such as an incorrect name or VAT number were legally insoluble. This is because the Act prohibits the issuing of more than one VAT invoice for a supply of a product or service. In terms of the law, a deduction for VAT is not allowed if there is an error (even a technical error) on the invoice.

The solution

An amendment to the VAT Act allows a corrected tax invoice to be issued. This needs to be done within twenty one days after the customer has requested a correction.

In addition, the vendor must keep an audit trail of the correction in case of a SARS query.

What has also been welcomed is that there is no change to the date of the transaction i.e. if the invoice was issued in January but corrected in February, the date the transaction is to be accounted for is still January.

An outstanding question and a checklist for you

This change to the VAT Act has brought certainty to an issue that has bedevilled business. One aspect that is still not clear is whether a business can issue a manual correction if its systems do not allow for an invoice to be electronically altered?

It is also worth remembering the legal requirements of a VAT invoice. They are that the invoice must contain:

- The words “Tax Invoice”, “VAT Invoice” or “Invoice”

- Name, address and VAT registration number of the supplier

- Name, address and, where the recipient is a vendor, the recipient’s VAT registration number

- Serial number and date of issue of invoice

- Accurate description of goods and/or services (indicating where applicable that the goods are second hand goods)

- Quantity or volume of goods or services supplied

- Value of the supply, the amount of tax charged and the consideration of the supply (value and the tax).

|

|

SARS Warns Taxpayers: “Use Only Registered Tax Practitioners”

|

There are no major tax deadlines for March but SARS is again warning taxpayers to –

- Only use registered Tax Practitioners,

- Ask for the practitioner’s registration number, and

- Verify the number online here.

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|