|

|

| |

|

July 2021

|

Buying Property from a Company – Should You Buy the Shares or the House?

|

|

"There is never a wrong time to buy the right home" (Anon)

You find the house of your dreams, agree on the price and get ready to put pen to paper. The house is in the name of a company, and you are offered a choice – either buy the house out of the company or take over the company (which owns the house and nothing else) by buying the shares and thus avoid the delay and cost of a normal property transfer and registration in the Deeds Office.

What should you do? There are a host of both practical and legal factors to consider before deciding. Holding property in a company can come with significant advantages, but there can also be major disadvantages, so professional advice specific to your own circumstances is a no-brainer here.

Some of the many factors you should consider are –

- Tax and estate planning considerations. These are complex and no two cases will be identical, but consider the higher capital gains tax rates payable by companies (and the annual exclusion and “primary residence exclusion” of R2m for individuals), the differential income tax rates, possible VAT considerations, your own estate planning circumstances (including the estate duty angle) and the like.

- Asset protection. Particularly if you run your own business or are in a profession at significant risk of litigation, it may be important to you to protect your major assets (like your house) from possible attack by creditors. Any assets held in your own name will be a natural target if you run into financial problems, whilst those held in another entity like a company or trust will generally be much harder to attack. Complicated multi-level structures such as having a trust owning your company’s shares have generally fallen out of favour for a variety of reasons, but you may still be advised to consider one in your particular situation.

- Joint ownership. Joint ownership of property comes with its own set of risks and issues, and depending on your needs you might be advised to address them with a company/shareholder structure.

- Costs and simplicity. Running a company comes with extra costs (accounting/auditing, statutory costs etc), formalities and responsibilities, getting a bond in your own name is likely to be a simpler process than taking it in a company, and so on.

- The hidden risks. When you buy a company’s shares you get the company as it is, with all its assets and liabilities. If the seller is in any way unreliable, you could find yourself losing the house to an undisclosed company liability that suddenly crawls out of the woodwork. Suretyships are a particular danger here – there is no central register of suretyships you can refer to, and it is common for groups of companies and other entities in particular to sign cross-suretyships without necessarily keeping a record of them all. These are risks that can be largely managed with proper advice and due diligence, but a residual whiff of doubt is inevitable.

- Other factors. There will be many other aspects to consider, depending on your circumstances and needs, and on the company in question.

Transfer duty - you pay it either way!

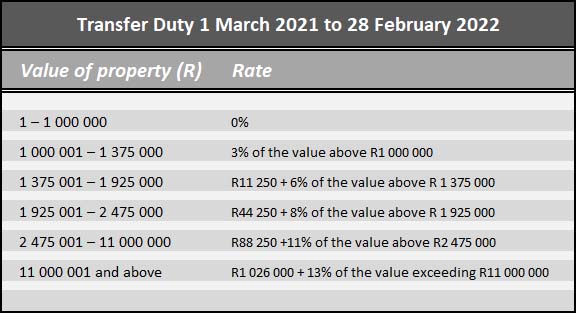

As a buyer you can never lose sight of all the costs you will incur in buying a house, and the “big one” is normally transfer duty. It’s essentially a government tax, payable by you as buyer (unless the property sale is subject to VAT), and it can be a lot of money.

Do not however fall into the old (and surprisingly still-common) trap of thinking that by buying the company you avoid paying transfer duty. That was indeed a commonly used loophole in decades past and it is still sometimes referred to. But in reality that all changed many years ago, and (subject to what is said below) you should budget to pay transfer duty as set out in this table -

Source: SARS “Budget Tax Guide 2021”

So for example if you buy a house for R3m you will pay R146k in transfer duty. Or R916k on a R10m house. Finding a way to avoid or reduce such a cost is an attractive proposition, and indeed until 2002 it was a common way for buyers and sellers to save transfer duty and to instead pay only ¼% “Securities Transfer Tax” – a huge saving.

That loophole closed however many years ago - on 13 December 2002 to be precise - and since then the sale of shares in a “residential property company” (a company with over 50% of its asset value in residential property) attracts transfer duty on the “fair value” of the property. No savings there!

What about “buying” a property-owning trust?

Similarly, before 2002 a common transfer duty avoidance strategy was to hold property in a trust, then to “sell” the trust to a purchaser by substituting him/her as a beneficiary of that trust. That loophole was also closed in respect of beneficiaries holding “contingent interests” in the property – the situation here is a bit more complicated than it is with companies as there are various types of trust you could be dealing with, so specialist advice is essential.

|

|

Spousal Maintenance After Divorce and the “Clean Break” Principle

|

|

“The clean break principle after divorce has found resonance with our courts for many years. The aim of this principle is to ensure that the parties become financially independent of each other as soon as possible after divorce.” (Extract from judgment below)

Our courts always prioritise the interests of children in any marital breakup, and child maintenance orders are accordingly tailored to ensure that both parents honour their obligations to support their children financially - to the extent that each spouse is able to do so, and for so long as is necessary.

Spousal maintenance on the other hand requires a more delicate balancing act. In a nutshell, spouses have a “reciprocal duty” to support each other during the marriage, and although that duty ends when the marriage ends, courts still have a wide discretion to order either “permanent” or “rehabilitative” maintenance of the financially weaker spouse by the financially stronger spouse.

Let’s have a look at a good example of how this discretion is applied in practice -

A bitter divorce and a claim for “permanent” maintenance

- A couple were married “out of community of property with accrual”.

- Their eventual divorce action required the Court to adjudicate a litany of bitter disputes, allegations and counter-allegations of misconduct and abuse.

- Whilst for our purposes we’ll concentrate on how the Court addressed the wife’s claim for “permanent maintenance” and the husband’s (reluctant) counter-offer of “rehabilitative maintenance” for a limited period of time, it is important to note that the maintenance issue was decided against the background of the other financial benefits awarded to the wife. She received 50% of the “accrual” in the estate, including a house, pension, and annuities – i.e. she did leave the marriage with a capital sum of money.

- The wife had previously been granted an interim order of maintenance of R6,500 p.m. “pendente lite” (“pending the litigation”). At the divorce hearing she argued that her chances of ever becoming self-supporting were slim given her age, health, outdated qualification, and limited exposure in the open labour market.

- Her husband on the other hand argued that she had “numerous skills and talents and has the potential to secure employment and earn a salary to support herself which when coupled with what she will receive from the accrued estate constitutes ample income to enable her to become self-sufficient.” Moreover he would retire in two years and his income would seriously decline as he would be dependent on his pension for his own support.

- Before we consider the legal aspects, an important factual finding by the Court was that the wife did indeed have at her disposal “numerous administrative skills and talents which will enable her to secure future employment”, and that there was no medical evidence to suggest that she could not find employment.

The law and the maintenance order

- As the Court put it: “The clean break principle after divorce has found resonance with our courts for many years.The aim of this principle is to ensure that the parties become financially independent of each other as soon as possible after divorce. This principle however has to be applied with due consideration of the particular circumstances of each case and if such circumstances permit.”

- The parties, said the Court, clearly wanted to “cut all ties and put an end to the marriage. In these circumstances, achieving a clean break finds resonance with this court.”

- Its conclusion: “Consistent with [the] principle of a clean break that resonates through our judgments, it is incumbent upon this court to equip the plaintiff to live independently of the defendant and to focus on developing and empowering herself to secure and sustain her future. In the circumstances, I am of the view that the required result which is the ultimate self-sufficiency of the plaintiff will be achieved by rehabilitative maintenance. I am further of the view that a proper analysis of the rationale behind the awarding of rehabilitative maintenance will conclude that an arbitrary period of the payment of rehabilitative maintenance will not address the ultimate achievement of self-sufficiency. A two year period of rehabilitative maintenance is justified in the circumstances.” (Emphasis supplied).

- For a period of 24 months after the divorce therefore, the husband must pay rehabilitative maintenance of R8,000 p.m. in addition to keeping his ex-wife on his medical aid and paying all her medical expenses.

|

|

R4m Damages for a Workplace Sexual Assault

|

|

“The stance adopted by the Municipality at the trial demonstrated a disturbing lack of appreciation of its legal obligation to have provided E[….] with a safe working environment.” (Extract from judgment below)

Our courts do not tolerate any form of sexual assault or harassment in the workplace and a recent High Court decision confirms the danger to both employees of engaging in this form of misconduct, and to employers of failing to address it.

The sexual assault and the damages claim

- In 2009 a “vibrant 23 year old woman” employed by a municipality as a clerk was sexually assaulted by her immediate superior, a Corporate Services Manager.

- The assault was described as follows: “As she looked up he bent down with his head over hers and, putting his mouth over hers, attempted to force his tongue into her mouth.She clenched her teeth and tried unsuccessfully to push him away.After a minute or so he desisted, leaving her with a mouthful of his saliva.She immediately wiped the saliva off her mouth. He then also tried to wipe her mouth with his hand but she knocked it away.” Importantly, the Court noted that that this was in no way just an attempt to “kiss” the victim; it was very far removed from a “kiss” and was instead a sexual assault.

- The victim subsequently resigned from her job “after her employer had made her employment intolerable compelling her to resign” and then for a variety of reasons decided to sue for damages for unlawful dismissal in the High Court rather than claim for unfair constructive dismissal via the CCMA (Commission for Conciliation, Mediation and Arbitration). Both avenues are available to any victim of such misconduct, and many factors will determine the best choice in any particular case.

- Thus began what proved to be the start of a long and gruelling saga, leading firstly to a 2016 High Court finding in the victim’s favour that her employer and the manager were both liable to her for “such damages as she may be able to prove she has suffered in consequence of the sexual assault upon her”.

- Back to the High Court went the victim to prove her damages. She had, held the Court after hearing all the evidence, been “deeply traumatized, she suffered from post traumatic stress disorder requiring extensive psychotherapy and “the course of the life of the deeply traumatised 34 year old woman who testified at the trial on quantum in late July 2020 had been much changed as a result of the assault.”

The employer’s “supine approach of bovine resignation”

- The Court hauled the employer over the coals as it “took no responsibility for its conduct and denied liability at the trial. At no stage did it apologize for the tremendous suffering it had caused E[…]. … It exhausted every avenue open to it to avoid having to compensate E[…] for the wrong which she had suffered at its hands.”

- Although the manager was found guilty of gross misconduct at a disciplinary enquiry, his sanction was a two-week suspension without pay rather than dismissal, an outcome described by the Court as “mindboggling given the character of the offence, the circumstance that [the manager] had abused his position of authority by assaulting a female subordinate who was in a particularly vulnerable position in that she was a temporary employee at the time that the assault occurred. Furthermore [the manager] did not demonstrate any remorse, remaining defiant to the end. Where an employee has been found guilty of gross misconduct and fails to take the first step towards rehabilitation by acknowledging his wrongdoing, there can be little scope for corrective or progressive discipline.” (Also relevant - the manager had received a suspended sentence of imprisonment after the victim laid charges against him, and he was already on a final written warning for theft from his employer.)

- The employer’s “approach of washing its hands of the matter, á la Pontius Pilate, fell woefully short of what was required of an employer in the circumstances. The Municipality abdicated its responsibilities to protect E[…] and adopted a supine approach of bovine resignation” (emphasis supplied).

- There was much more from the Court in the same vein – the employer had, “through protracted litigation, made her wait so long for justice, thereby adding to her suffering …On a human level, the defence which was put up by the Municipality was devoid of introspection, humility or compassion … it had lengthened and intensified the trauma suffered by E[…] … there was no, as it were, corporate repentance ... The Municipality was quick to defend the litigation and slow to listen to E[…]”.

The end result – the employer and the manager must “jointly and severally” pay to the victim a total of R3,998,955.02 in damages for loss of earnings, psychological/medical expenses, and general damages. They are also in for (doubtless substantial) legal costs, including the costs of four expert witnesses.

|

|

Bodies Corporate: Before You Sequestrate to Recover Arrears…

|

|

“Bankruptcy - a fate worse than debt” (Anon)

One of a Body Corporate’s fundamental duties is to collect monthly levies from the scheme’s members, and to take robust action to recover any arrears. As with any other creditor/debtor relationship however, trying to recover debt can be an exercise in frustration and delay, and the more recalcitrant the debtor, the greater the temptation to “go straight for the jugular” by applying to sequestrate the debtor’s estate.

You will have to show that the sequestration is to the advantage of creditors as a whole – not just to you - but that isn’t the only consideration. You will be throwing good money after bad if you end up having to pay a “contribution to the costs of sequestration”.

The recent case of a sectional title Body Corporate, which perhaps thought that it was protected from this particular danger because of its statutory preferences for recovery of arrear levies prior to transfer, illustrates the danger.

But before we get to the facts and the outcome of that case let’s have a quick look at the general principles involved.

What is a “contribution to costs” and who has to pay it?

If you want to share in the net proceeds of an insolvent estate, you must formally prove your claim at a meeting of creditors convened by the trustee of the insolvent estate. If you don’t do that, you wave goodbye to any possible dividend and will be writing off the debt.

On the other hand, if you decide to prove your claim you may be at risk of having to pay into the estate as well as writing off the debt - talk about adding insult to injury! That danger arises if the costs of sequestrating the estate exceed the funds in the estate available to pay them. In that event the trustee of the insolvent estate will recover a “contribution to costs” from proved creditors – including you if your claim was proved as above.

The special danger of being the “petitioning creditor”

The creditor who applies for the debtor’s sequestration is - as “the petitioning creditor” – liable to contribute to the shortfall even without proving a claim. In other words, unlike other creditors, you cannot protect yourself from contributing to costs by holding back the claim – you are “deemed” to have proved it. That’s why, although applying for sequestration can be an excellent way of recovering debt from a recalcitrant debtor, it is essential to first consider the danger of contribution.

How “secured creditors” can protect themselves

Also relevant to our story is that a creditor holding security (such as a bond over the insolvent’s property) must prove its secured claim in order to be paid out the net proceeds of its security. A secured creditor can, if it suffers a shortfall after being paid out those net proceeds of its security, also share in the “free residue” of the estate. The “free residue” is the net proceeds of all unencumbered assets available for distribution to creditors. The secured creditor’s share in this event will be based on the “concurrent” portion of its claim, in other words it is now a concurrent creditor.

This is where the danger comes in because any contribution payable is payable in the free residue by concurrent creditors. A secured creditor can largely protect itself from this danger by “relying on the proceeds of its security” to satisfy its claim. By doing so it waives its concurrent claim for the shortfall, but equally it no longer has to contribute along with the other proved (or petitioning) concurrent creditors. It will now only have to contribute when there are no other such creditors, or when other contributors are unable to pay their share.

The case of the Body Corporate that sequestrated to recover arrears – and paid the price

Let’s see how those principles were applied in a recent Supreme Court of Appeal (SCA) case -

- The owner of two sectional title units, bonded to separate banks, was unable to pay his levies. The Body Corporate sequestrated his estate, and his two units were sold. Only the two banks proved claims.

- This was where the Body Corporate’s statutory protection for arrear levies came in. No transfer can be registered in the Deeds Office until all rates and taxes (and levies in the case of Bodies Corporate and Homeowners Associations) have been paid in full. Thus the arrear levies were paid in full to the Body Corporate by the transferring attorneys. “Done and dusted” thought the Body Corporate, but it was not to be.

- There was a shortfall in the insolvent estate, and the trustee tried to recover the resultant contribution from the two banks (the bondholders) who had proved their claims in the estate.

- The banks objected, arguing that because they had relied on their security in proving their claims, they were not liable to contribute (as above). The Body Corporate, they argued, was as the petitioning creditor liable for the contribution despite not having proved its claim.

- The Body Corporate on the other hand argued that it could never be liable for a contribution. Although it was indeed the petitioning creditor, it had never proved a claim against the estate and the arrear levies had been paid to it in full, as required by law, before transfer of the properties.

- To cut a long story short, the dispute wound its way through our courts and ended up in the SCA, which, after a detailed examination of the relevant law, held the Body Corporate as petitioning creditor to be solely liable for the full amount of the contribution to costs (R46 663.16).

Bodies Corporate beware!

The Court’s reasoning in reaching this conclusion will be of great interest to the lawyers amongst us, but the bottom line for Bodies Corporate is this – if you sequestrate to recover arrears, you could well end up carrying the full brunt of any contribution to costs.

So perhaps take advice on whether you can/should rather use other debt collection processes, including perhaps applying to the CSOS (Community Schemes Ombud Service) to order and enforce payment of the arrears.

|

|

Your Website of the Month: How to Plan and Hold Virtual Board Meetings

|

|

Virtual meetings are here to stay. Make the most of them with “Optimising the virtual boardroom: A guide to planning and executing virtual board meetings” from Nasdaq Governance Solutions on Moneyweb.

Learn how to –

- “Build a virtual board table” (“creating a virtual seating arrangement” and so on),

- “Mitigate meeting day glitches” (we’ve all wasted time on fiascos!), and

- “Keep it confidential” (paramount).

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|