|

|

| |

|

January 2023

|

Start 2023 Strong with the “Fresh Start Effect”

|

|

“We change our tools and then our tools change us.” (Jeff Bezos)

Every January, individuals and businesses have an opportunity to take advantage of what is called the “Fresh Start Effect” – referring to research evidence that shows people are more likely to make positive changes at times that mark the start of a new time period and represent a new beginning, most notably the start of a new year.

With the right tools, businesses can maximise this Fresh Start Effect to begin the new year on a strong footing. Three business tools, in particular, are indispensable to achieve this: a business review; goals and a plan for the year – including a budget; and ways to measure progress in achieving goals and executing the plan in the months ahead. Fortunately, these tools are not expensive or difficult to use, and your accountant will be able to assist you to set your business up for great results in 2023.

- A business review

A comprehensive review of business operations is a simple but powerful business tool.

It enables business owners and managers to analyse performance in achieving goals and meeting key performance indicators (KPIs), and to identify problems and spot trends timeously. Most importantly, an effective review will reveal what is working and what is not, so the team can celebrate successes and build on what is working, and also change what is not working to get better results.

Some of the business areas that need to be reviewed may include:

- Business plan, sales, marketing and branding strategies.

- Total income to total expenses, cash flow statement and debtors’ reports, actual vs budget spend, and the balance sheet.

- Internal resources including the company’s people and processes.

- Client base, client processes and customer satisfaction.

- Statutory and regulatory compliance.

- Fees, contracts and costs.

The best way to do a business review is to involve your entire team and to call in professional assistance for a clearer understanding, particularly of the financial aspects of the review.

- Goals and a plan for 2023, including a budget

The business review will provide invaluable information and insights, creating a baseline from which goals can be set for the next 12 months. This enables planning for the year ahead, incorporating the necessary changes to get better results, as well as enhancing or duplicating the processes already generating good results.

Goalsetting, as well as planning and budgeting to achieve these goals, are great tools for establishing the direction of the business for the next year, focussing the team’s attention and efforts, and improving the chances of success.

SMART goals are always the most effective – these are goals that are Specific, Measurable, Achievable, Relevant, and Time-Bound. That is because SMART goals are clear and quantifiable and can be broken down into a plan that details the specific steps or milestones to be completed - and the budgets within which to do so.

- Measuring progress during the year ahead

Measuring progress ensures both better management and greater motivation. What is measured can be managed, and progress on all business goals can be measured through, among others, regular and up-to-date financial reports, (KPIs) and project management tools.

KPIs, for example, are like scorecards that track performance against business goals and can be an effective tool for keeping team members motivated during the year. Experts suggest that smaller businesses should start by measuring only a few KPIs in the crucial business areas of income; customers; employees; and processes; but your accountant will be able to provide invaluable advice for your specific business.

Similarly, there are different project management tools for various types of projects or management approaches. Benjamin Franklin’s advice may be helpful here: “The best investment is in the tools of one's own trade.”

This January, take advantage of the “Fresh Start Effect,” by reaching out to your accountant for advice and assistance in using each of these business tools to set your business up for a great 2023.

|

|

The Financial Steps You Need to Take Before You Open Your New Business

|

|

“Good fortune is what happens when opportunity meets planning,” - Thomas Edison

You have your idea, you have your mission statement and perhaps you even have an idea of who your first customers will be, but there are still a few things you should consider doing before you launch your company. When it comes to your finances doing these five things in advance will ready you and your business for success and allow you to focus more on the company and less on the necessary financial administration.

Deal with your personal finances

For some entrepreneurs starting a company is seen as a way to get themselves out of financial trouble. Unfortunately, if this is the case, the company will be starting off on the back foot. If your motivation for starting a business is as a way to repay your own loans or debts, then you won't be making the best decisions for the company. Ideally, your finances should be clean with debts paid off and taxes up to date. This will allow you to focus on the company for what it is, rather than on what you need.

Ideally, you will be starting your company with your own personal finances sorted for the first six months at least, and with no debt. If you are in trouble, or don't have any savings, then it is important that you get any loans and debts under control and reshape your personal expenses in line with leaner times before you take your first new business step.

Consolidate any debts you may have and arrange for lower monthly payments. Cancel any unnecessary services and costs and try to get your monthly outgoings as low as you can before you quit your job or start your company. You are going to have tough months and it's important that you are ready to weather them if you hope to succeed.

Open a business account

Many new businesses begin as extensions of the owner. Sometimes the owner's finances are used to pay for business expenses and these costs get lost along the way in the search for success. It is therefore important to decide on a vehicle for your business (ask your accountant to advise you on whether you will be best off with a company, trading trust, or sole tradership) then open a business banking account to more accurately keep track of exactly what is owed by your business to you, or you to your business. All relevant business expenses are tax deductible, but this can't happen if they aren't accurately tracked and accounted for in the business. Opening an account will help you not only look more professional but also track your income and outgoings more effectively.

Get your taxes up to date

Your personal taxes are an important aspect of business leadership. If your taxes are not properly filed and up to date when you have a job, the chances are they are only going to get worse. Ask your accountant to look at your personal situation and ensure everything that is owed is paid and signed off.

The good news is that at the same time you can also ask your accountant to look at your business and advise you on how best to structure things to get the most from the money you are earning. In the early days, every cent is going to count, and you will want to wring every benefit possible out of the company to get it launched. You don't want to be paying more tax than you are required to.

Take a basic finance course

Everything these days can be learnt online. Whether you take a formal course or watch a series of YouTube videos, it is highly advised that you learn the basics of finance, especially if you have never worked in that department before. While working with your accountant is an important step when starting any new endeavour, it is also important that you understand the basics of what is going on day-to-day when it comes to pricing, sales, expenditure, profit and loss. Without this knowledge you won't be able to make the important decisions that can make or break a company.

Set up automatic invoicing

Many small business owners opt to use Word and Excel invoice templates when starting out, but these require manual entries, can be time consuming and are difficult to track. A recent study also revealed that 39% of invoices are paid late and 61% of late payments are as a direct result of invoicing errors.

Do you know which invoices have been sent out, which have been paid and which are outstanding? There are many automated invoicing systems, which will take the worries out of invoicing and allow you to track payments and due dates. This in turn helps you to keep track of cash flow and ensure that you always have the money necessary to pay your expenses.

Invoice automation systems can also offer automatic reconciliation, generate recurring invoices and even capture data on expenses from photographs of receipts. Importantly you can also generate automatic reminder emails to chase up payments and make your monthly payments automatically, too. The time and stress savings are enormous and at the end of the day you will be able to hand over organised and presentable books to your accountant, enabling them to file taxes and notice potential areas for savings more easily.

|

|

The Importance of Maintaining Your Tax Compliance Status in 2023

|

|

“Being tax compliant… is not just good for you, but also contributes to the positive growth of our country’s economy which in turn benefits all South Africans.” (SARS)

Businesses are often required to provide, confirm or share tax clearance information to another entity. This is because proof of tax compliance is an indicator of a company’s good standing in terms of its legal obligations and how well it is managed. There may be instances when an individual, another company, or a government entity needs to verify your tax compliance status, for example, during a prequalification as a supplier; for a tender application or bidding process; to confirm good standing and that your tax matters are in order with SARS; or for foreign investment allowances.

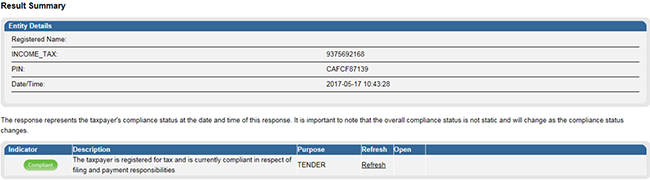

Tax clearance information is no longer confirmed via Tax Clearance Certificates – these have been replaced by SARS’ Tax Compliance Status (TCS) system, which verifies your tax status online and in real-time, and makes it very important to ensure you and your company are always compliant.

How it works now

Instead of a manual tax certificate being issued as in the past, SARS’ new system allows individuals and businesses to obtain a TCS PIN (personal identification number).

Your accountant will be able to assist with the process of applying to SARS to obtain this PIN through eFiling which requires, for example, activating the TCS for the business or individual, merging all the tax types into one registered profile, completing the Tax Compliance Status Request and selecting the correct type of TCS: good standing, tender, or – for individuals only - emigration and foreign investment allowance.

If all your tax affairs are in order, your PIN should be issued immediately via SMS or email. A unique PIN is issued for each TCS request submitted to SARS.

This PIN, along with your tax reference number is then sent to the third-party that requires confirmation of your or the company’s tax compliance status. To verify tax compliance status, the third-party will go to eFiling and submit your tax reference number and PIN under “New Verification Request.”

Your current tax compliance status will appear and will be colour-coded, indicating if your tax affairs are currently in order or not:

- green indicates that all tax affairs are in order and the taxpayer is tax compliant;

- red means the taxpayer is not tax compliant.

Click here to see full size screenshot

Source: SARS

It is important to note that the PIN is valid for a year and will reflect the current tax status at the date and time the PIN is entered into the TCS system (not the compliance status at the time the PIN was issued).

This means your tax compliance status on the system can change during the year in line with your tax behaviour, which might include, for example, an inadvertent late submission or missed payment. For this reason, it is crucial to continuously monitor your tax compliance status to ensure a non-compliant tax status does not impact business and other opportunities.

What is required to be tax compliant?

SARS says that the compliance status displayed reflects the following compliance requirements:

- Registration for all required tax types

- Submission of all required tax returns on time

- All tax debt settled on time

- Relevant supporting documents submitted.

To meet these requirements consistently across all the relevant tax types over the tax year, taxpayers should consider professional assistance.

Why it is so important to maintain compliance all year round?

- Remember that a TCS PIN is valid for a year and third parties with whom you share the PIN will always see your current tax compliance status, so it is crucial to ensure that status is continuously monitored and is compliant at all times during the year, to avoid a negative impact on reputation and opportunities.

- A non-compliant status can affect the confidence of potential clients, stakeholders and investors, as well as competitiveness in the market.

- Continuous compliance does involve costs or resources but will never be as expensive as the costs associated with non-compliance, which generally involve both penalties and additional fees to rectify.

- Non-compliance exposes taxpayers to wide and harsh collection or enforcement measures such as the confiscation of property, business closure, garnishee orders and agency notices. Some tax offences are also subject to custodial sentences.

- Ongoing and consistent compliance all year means that when there is an instance of non-compliance, SARS will likely be more accommodating, because a taxpayer’s track record is one of the factors SARS considers when making determinations.

- Maintaining a compliant tax status prevents tax surprises and enables lawful tax planning as well as the ability to take advantage of relevant rebates and incentives.

|

|

How to Know if You Need an Office for Your Business (and How to Make the Most of a Lease if You Do)

|

|

“In business, you don't get what you deserve, you get what you negotiate,” Chester Karrass, Founder of Seminar group Karrass.

At some point, around halfway through the pandemic, experts began to whisper that office space was dead. “No one will be using an office by 2023,” they said. And yet, while it's true that office space use has declined steeply in some parts of the country, many companies are still finding a use for a dedicated environment in which to conduct business.

Do you need an office for your business?

Remote work has proven that the humble office we remember is not essential, but there are still several functions an office can serve. For many employees, an office can serve simply as a distraction-free environment in which to work, while for others it may cement team relationships. For others, it can be a way to separate work and home lives. Employees also often need physical meeting spaces, a place to pore over designs and showcase physical models. Moreover, introducing new employees is easier in a formal physical office space, as is hosting company celebrations.

Despite this, remote work has seen a decrease in demand in many parts of South Africa and given this there has never been a better time than now to negotiate for that dedicated office space if you find that your company needs it.

These tips will help you get what you need.

Get the right amount of space

Here's a quick guide to getting the space you need and no more:

- Conference room (15 to 30 people): 75 to 90 square metres

- Small meeting room (2 to 4 people): 30 square metres

- Large meeting room (4 to 8 people): 45 square metres

- Manager's office: 25 square metres

- Senior Manager's office including private meeting table: 50 square metres

- Server room (1 to 4 racks): 12 to 40 square metres.

In addition, you will need roughly 30 square metres of space per employee. This may adjust upward dependent on the kind of work you do (do your employees need to spread plans out on their desks for instance?) or downward if employees are hot-desking and not expected to be in the office each day. Finally, remember your future expectations. If the plan is to hire more people shortly, then they should be catered for as well. No use incurring the cost of moving in a few years if you can avoid it. For a more accurate picture that includes what you need, try this office space calculator.

Consider also the “hive” or “shared office space” alternatives on offer in some cities.

Other facilities

When renting an office, you may want to consider a variety of factors that don't include size. How easy is the office to travel to? Is there traffic and easy access to public transport? Does the block have a generator or solar for loadshedding? Do you need access to printing shops or mailing? What sort of hours will you be open, and will employees need night security and parking? Will your employees need food stores nearby, or are you catering for them?

The rent is only a part of the cost

Most people will want to exclusively look at the price per metre in rent, but remember, while important the monthly rental is only part of the cost. What will you pay for water, lights, security and internet? Can you afford the phone charges? What is included in the rental? Are you responsible for building maintenance or renovation? Is there an allowance for any renovation that might be needed before you take occupation? Refuse removal costs? What about the cost of furnishing a new building? Will you need to change the carpets or put-up signage on the building? Now is the time to bring in an accountant to help you work out the true cost of your office.

Negotiate

Do not assume that the rent or the terms of the rental agreement are set in stone. These days there is a lot more supply than demand so those who are leasing have the option to ask for rent decreases and favourable terms and conditions.

At this stage, it may be wise to bring in a professional to look at the terms of the contract and negotiate for you. Remember, the party that wins in these situations is always the one who is prepared to walk away.

The ongoing level of rental (and agreed rates of escalation) are likely to be your focus when negotiating the best deal but other negotiation points could include:

- Maintenance of the building – who is responsible for what?

- Length of the term – if you plan a long-term rental, many landlords could be open to lowering the initial rental, perhaps even granting an initial rental holiday, and/or to carry some of your other costs beyond rental.

- Amenities (such as internet, water or electricity) might be included in the bill.

|

|

Your Tax Deadlines for January 2023

|

- 6 January - Monthly Pay-As-You-Earn (PAYE) submissions and payments

- 30 January - Excise Duty payments

- 31 January - Value-Added Tax (VAT) electronic submissions and payments & CIT Provisional payments where applicable.

|

|

|

Have a Healthy,

Happy and Successful

2023!

|

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|