|

|

| |

|

January 2020

|

What Will The Next Decade Bring Us?

|

“If we can win the Rugby World Cup three times, surely it is not asking too much of this country to take the High Road twice when its future is on the line? When push comes to shove, ordinary South Africans can do extraordinary things!” (Clem Sunter)

The major global trends that have recently emerged and are widely predicted to continue to dominate the world are:

- A rising tide of nationalism and anger at the status quo which manifests itself in trying to stop immigration into Western Europe and the United States, an increasing move away from free trade and more and more civil unrest. If you put all this together, it will result in slower global economic growth and rising tensions within countries and conflicts between nations (India and Pakistan, Turkey and the Kurds/Syrians, the USA and Iran to name a few).

For South Africa, which is dependent on growing trade, this will put more pressure on an already struggling economy. Civic unrest is also a significant trend here and hopefully we can recreate the 1990s when we stunned the world by negotiating a peaceful transition to democracy.

- Superpower tensions as China vies to overtake the USA both economically and militarily. Russia is also showing global ambitions. So far this has played itself out in US tariffs against China and sanctions on Russia, but you can expect this to hot up.

South Africa is a long way from these battle grounds and should be spared any conflicts that arise. In fact, we will probably benefit as the superpowers vie for influence which should translate into investment into our declining infrastructure.

- The last decade has been characterised by easy money and low interest rates, which opens the distinct possibility that there will be another economic crash similar to the one in 2008.

This would not be good news for South Africa as our economy is already stretched by rising debt. We survived the last crash well as we had strong economic fundamentals and were able to fight the effects of the crash with an economic stimulus program but now we have no leeway to counteract a global recession, should there be a crash.

Another factor is whether we will drop to full junk status which will be detrimental to the economy.

- Shadowing and shading everything is climate change which has arrived and is making itself increasingly felt. Already we have seen how a disastrous drought was one of the causes of the Syrian civil war and we know how dry parts of South Africa are. Rising levels of carbon dioxide are making the world hotter (already temperatures have risen by 1 degree centigrade and continue to rise) – if temperatures rise half a degree, it will cost the world $56 trillion to deal with the effects.

The problem with climate change is that it compounds all the above problems like rising numbers of refugees, less food etc. Desertification will drive more people into crowded cities along with more extreme weather events.

More and more climate change specialists are saying we are getting closer to a tipping point whereby climate change becomes irreversible. Why don’t we all commit in our own small ways to reduce the carbon emissions we cause and to look to ways to conserve water?

None of our problems are insurmountable!

Although we are clearly going through increasingly risky global and local times, none of our problems are insurmountable. With will and a spirit of compromise we can achieve surprising things – nobody realistically expected South Africa to win the Rugby World Cup, but we did.

|

|

Your Tax Returns Are Due: Make Sure You Fill In Your Return Correctly

|

“The hardest thing in the world to understand is the income tax” (Albert Einstein)

Provisional taxpayers using eFiling need to have completed and submitted their 2019 income tax return on or by 31 January.

Make sure you are prepared for this and don’t underestimate the time needed to put the return together. As a starting point you should have a good filing system which makes it easy to find documentation needed to both fill in the return and upload to SARS in terms of supporting schedules.

The income tax return form runs to more than thirty pages, so there is plenty of work to be done – don’t leave it to the last minute!

Your return must be complete

The onus is on you to satisfy SARS that your return is comprehensively and completely filled in. Thus, even if you supply SARS with all the documentation and explanations required, not ticking a box in the form that is applicable can lead to SARS deducing that you have not met your obligation of full disclosure.

This is important as if SARS deems there to be a material non-disclosure in your return (remembering that SARS tends to apply a very narrow interpretation of this) then the three year prescription period for your tax return is waived and SARS can go back and start raising queries on your 2010 return for example. This can put you onto a nightmare road, so take extra care.

We are all aware that SARS has been missing its collection targets in recent years and is under enormous pressure to maximise revenue from taxpayers.

Your accountant is there to assist you – this is a good time to make use of his or her services.

|

|

How To Detect and Dodge Financial Scams

|

“If it sounds too good to be true, it probably is” (wise old adage)

In the USA, $40 billion is lost every year to scammers. When you consider statistics suggesting that 65% of scam victims don’t report their losses (usually they are too embarrassed to admit they have been conned), as much as $120 billion could annually be skimmed from gullible people.

Scammers normally target people who are financially vulnerable (they have lost their jobs or their business has folded) or they take advantage of economic downturns where a large percentage of people experience financial hardship.

The quick con

Typically, it is difficult to fully get to grips with the scheme they sell you as the scheme’s workings are hard to fully understand. But the conmen tell you that the real issue is you will get astronomical returns and they will show you for example pictures of yachts cruising in the Mediterranean – messaging you “this is the life you will lead once you have made your quick fortune”.

Because they prey on the financially vulnerable, the conmen spin conspiracy theories – the reason you have fallen on hard times is the system has crushed you and this scheme bypasses all the financial regulation “nonsense” – and the like.

Conmen are also hard salesmen and they will pressurise you into making this “investment”.

The long con

You need to be really careful of these as you are up against some sophisticated operators. The main principle is to get assurance from people in your social circle that the scammer or the scheme is credible and achieves high returns (these people are wittingly or unwittingly part of the con). In addition, the scammers can point you to well-known financial experts who will vouch for the scheme (they typically are part of the con).

It is usually a Ponzi scheme which will operate successfully until no new funds come into the scheme. It then unravels very quickly, and the vast bulk of investors lose their investments.

Another type of scam is “pump and dump” where salesmen extol a little-known share, and this drives the price up. These salesmen make aggressive pitches to unsuspecting victims who get carried away by the upward momentum of the share. Once the share has gone way over its value, the conmen sell it short (the dump of the scheme) and the share price collapses.

Who is vulnerable to these scammers?

Strangely enough it is often well-to-do people (usually men) who are experiencing financial stress and are happy to take on risk. These people are well educated and financially literate.

The combination of factors that makes them gullible is (apart from being under financial stress):

- Being put under pressure by the conmen (they need to get in “before it’s too late” and their friends “are making a killing”)

- The scheme can be complex or opaque and so they rely on their intuition

- Most of these people are decent and trusting, so they tend to believe the conmen and they don’t want to let the conmen down (no doubt the scammers are aware of this vulnerability)

- Emotional. Greed is a very powerful emotion and can lead to impulsive decisions which you will regret later.

Sir Isaac Newton was a great genius, but he lost all his money in the South Sea Bubble scam in the 1720’s.

So before you get caught up in a scam step back and think rationally. You should also analyse yourself and if you have any of the above traits, then be very careful of any investments that are “too good to be true”.

|

|

Junk Status Is Not The End - It Can Get A Lot Worse!

|

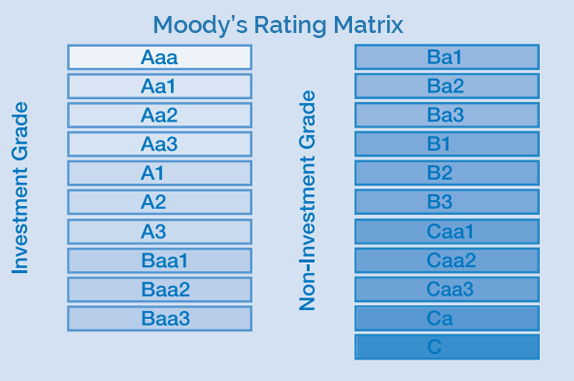

It is now widely expected that sometime in the next year or so Moody’s will downgrade South Africa’s debt to junk status. Many see this as the beginning of the process to rehabilitate ourselves. True, initially we will go through a difficult period as ±R150 billion of our debt will be sold as many offshore institutional investors cannot hold junk bonds which leads to a fall in the currency, higher interest rates and lower economic growth. But then we knuckle down and begin to reform the economy and embark on the process of returning to investment grade.

However - things can get much worse

|

Source : Moody’s

We are currently Baa3 with Moody’s and are on a negative watch with them which means they will put South Africa on Ba1 (i.e. junk status) if we don’t get economic growth on an upward path and rein in our rising debt.

As you can see, we can keep dropping to Ba2 and all the way down to C which means South Africa has defaulted on its debt obligations and there’s little prospect of recovery.

It can happen – just look at Venezuela and Zimbabwe – where optimistic assumptions are made on economic growth and government expenditure but in fact the country just raises taxes, incurs more debt, until you need to borrow money just to pay off debt that falls due. Each drop on the Rating Matrix raises the cost of borrowing and the downward spiral continues.

The ultimate problem with this scenario is that it eventually becomes irreversible, which is when default on debt becomes a distinct possibility.

The reality is that until genuine reforms are put in place, we will continue to descend along the Rating Matrix ladder.

What should we be doing?

Paying off as much debt as possible is a good start. We should also carefully consider any future expenditure and analyse just how necessary it will be, particularly if it is in foreign currency. Some analysts recommend that we should become as self-sufficient as possible (e.g. boreholes, solar power).

|

|

|

Your Tax Deadlines for January 2020

|

- 7 January – Monthly PAYE submissions and payments

- 24 January – VAT manual submissions and payments

- 30 January – Excise Duty payments

- 31 January – VAT electronic submissions and payments

- 31 January – CIT Provisional Tax Payments where applicable

- 31 January – 2019 Income Tax submission due for provisional taxpayers using eFiling.

|

|

|

“Have a Healthy,

Happy and Successful

2020!”

|

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|