|

|

| |

|

March 2020

|

Budget 2020: Some Tax Relief!

|

Taxpayers were preparing for once again being squeezed in 2020, but we have been pleasantly surprised as we have been given a myriad of tax concessions in this budget. In fact, the average taxpayer will be over 5% better off than in 2019/2020.

The Finance Minister has decided that taxpayers have borne the brunt of austerity for too long. Instead he has opted for R261 billion in cost reduction over the next three years – the bulk of which (R160 billion) will come from slashing remuneration of government and State Owned Enterprises (SOEs) staff.

Thus, Tito Mboweni surprised the market by taking on a holy cow – public servants’ remuneration. The real issue now is how the unions (remember they are key government allies) will respond. They have already rejected the Budget proposals, so some tough bargaining lies ahead.

The following proposed tax changes were announced

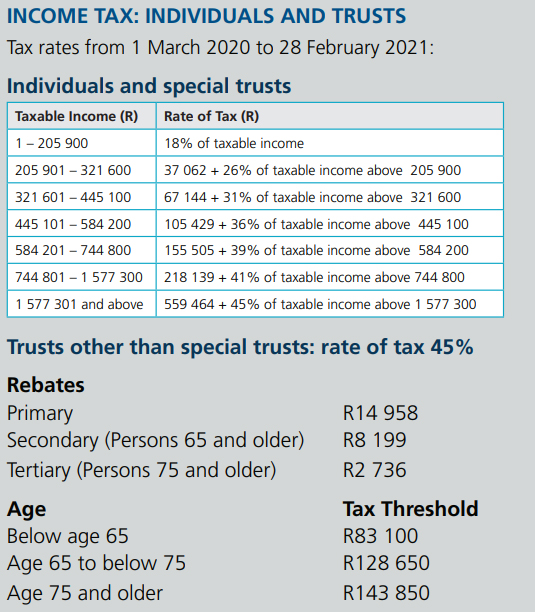

- Income tax rates are left unchanged. Tax brackets (and tax rebates) were favourably adjusted by R14 billion. This results in a net gain of R2 billion for taxpayers, as fiscal drag will amount to R12 billion (the amount that inflation would have pushed taxpayers into higher tax brackets).

A person earning R460 000 a year will now pay R3 400 less in taxes in 2020/21. The average saving per taxpayer is 5.2%.

This R2 billion loss to the government will be covered by R1.75 billion from Carbon taxes and R250 million from an increase in the plastic bag levy.

- “Sin” taxes have mainly had inflation-linked increases with beer, wine, spirits and cigarettes going up on 1 April (see tables below). Of interest here is that heated tobacco products (such as hubbly bubbly) will now be taxed at 75% of the excise rate on cigarettes and a vaping tax (E-cigarettes) will be introduced in 2021.

- Carbon Tax will increase by 5.6% from R120 per ton to R127 of carbon dioxide equivalent. Another “green tax”, the plastic bag levy has been increased to 25 cents per bag.

- The fuel levy will increase by 25 cents a litre on 1 April (16 cents for the general fuel levy and 9 cents for the Road Accident Fund).

- Medical tax credits will rise by R9 to R319 for the first two beneficiaries and by R6 to R215 for each additional beneficiary. This is also unexpectedly good news as the thrust of recent budgets has been to limit medical tax credits ahead of the introduction of National Health Insurance (there was very little in the Budget about NHI).

- Expat Tax – the amount of remuneration earned outside South Africa, that qualifies for exemption from normal tax will be increased from R1 million to R1,25 million. This is also a positive development.

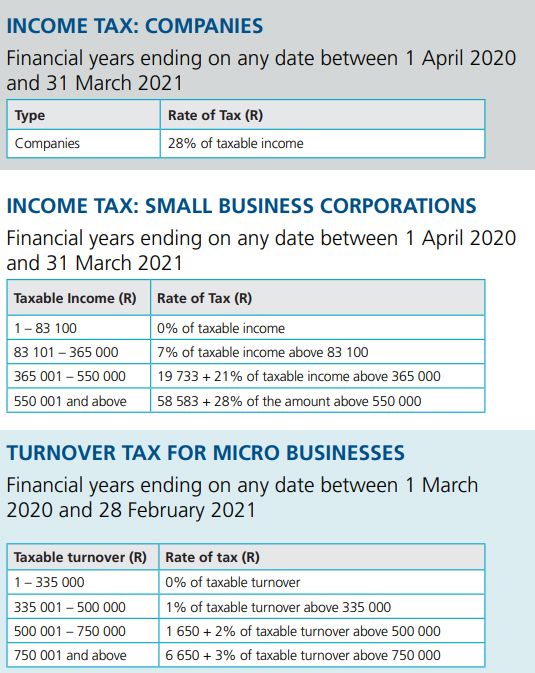

- Micro Business Turnover Tax. There is a marginal decrease in the Micro Business Turnover Tax, whilst Small Business Corporation Tax remains unchanged.

- The Transfer Duty Exemption has been increased to R1 million from R900 000, which means you will pay zero transfer duty on any property valued up to R1m.

- The Business Travel Tax Free Allowance has increased to R3.98 per kilometre (R3.61 last year).

- The annual limit on contributions to a Tax-Free Investment has been increased by R3 000 to R36 000.

The following tax rates are unchanged

- Value Added Tax at 15%.

- Dividend tax at 20%.

- Company Tax at 28% and Trusts at 45%. The Minister said amendments will be made to reduce certain exemptions, review and put end dates on incentives, limit the deduction of assessed losses to 80% of taxable income, ahead of announcing a drop in company tax rates to make South Africa a globally-competitive corporate workplace.

- All withholding taxes.

The following also remained the same

- The Interest Exemption on Income Tax - R23 800 if you are under 65 and over 65 R34 800.

- Retirement savings contribution limit remains at 27.5% of income.

- The inclusion rate applying to Capital Gains – the maximum rate at which normal tax on capital gains will be levied remains at 18% for individuals, 22.4% for companies and 36% for trusts.

Tax Tables - Budget 2020

|

|

Your Selection of Budget 2020 Tax Calculators

|

- How long will you work for the taxman today?

Input your salary into the 2020 Tax Clock calculator and find out how many hours you will spend today working for the taxman, and at what time precisely you will finally start working for yourself (warning – it’s not pretty!).

- How will your income tax change?

Put your monthly taxable income into Fin24’s Budget 2020 Income Tax Calculator to find out.

- How much extra will your sin taxes cost you this year?

Work out how much more you will be shelling out for spirits, wine, beer and cigarettes (or how much you will be saving if you don’t indulge!) with Fin24’s Budget 2020 Sin Tax Calculator.

|

|

Budget 2020: Will it Please Moody’s?

|

“Baby, baby, baby you’re out of time” (The Rolling Stones)

Over the past several years South Africa’s debt position has worsened considerably to the point where of the major ratings agencies only Moody’s has not downgraded us to junk status. They have made it clear that they are seriously considering such a move and will probably make the decision based on how they view Minister Mboweni’s budget.

One key to this is how the Minister approached restoring fiscal discipline to the economy. He has already stated that R150 billion in savings needs to be achieved in the next three years.

By cutting the wage bill of public servants by R160 billion (nearly R38 billion in the 2020 Budget) over the next three years, Minister Mboweni has achieved the required savings. But will the unions accede to this? Almost certainly not without a bloody battle and Mr Mboweni has acknowledged this is going to be a very challenging time. The key negotiations will happen mid-year, so Moody’s may wait for the outcome of these talks.

The second key to avoid a Moody’s downgrade is sustained economic growth - yet we had an estimated 0.3% growth in 2019 and 2020 is forecast at 0.9% (2021 at 1.3% and 2022 at 1.6%). Load shedding will continue for at least two more years and this considerably dims any realistic chance of there being any breakout of economic growth.

Even with the wage cuts announced national debt will continue to climb and by 2022/23 interest payments on debt will be approaching R300 billion or 18% of the budget (almost double what it was in 2014). Debt to GDP will be over 71% versus 61% now. This is exacerbated by the fact that an additional R112 billion has been allocated to SOEs of which R60 billion is for Eskom.

It is encouraging that government is now making concerted efforts to remove the impediments to economic growth but the problems such as a bloated public service, Eskom and structural problems like inadequate infrastructure, corruption and inordinate red tape have been around for years. Time doesn’t wait and as the song says “you’re out of time”.

Moody’s have already expressed doubt about how achievable the R261 billion cuts in public salaries are. Moody’s vice president Lucie Villa: “The authorities have yet to negotiate any moderation in wages with the country’s unions, which will likely be challenging given South Africa’s socioeconomic realities and would represent a significant departure from the outcome of previous negotiations.”

Tito Mboweni was brave to recognise that piling on tax increases is counter-productive and that urgent reforms need to be made but the general consensus seems to be that it is difficult to foresee any other outcome than a Moody’s downgrade.

|

|

Directors: “Knowing” Is A Potentially Career-Threatening Word for You

|

“An investment in knowledge pays the best interest” (Benjamin Franklin)

The Companies Act 2008 places onerous duties on directors and if you do not meet these obligations, you risk personal liability for any damages flowing from these actions.

“Knowing” in the company law context

A director gets “knowing” (actual knowledge) of the company by remaining apprised of the conditions of the relevant industry, what is revealed by the media of the business or its competitors and from the “pack” of data received before a directors’ meeting.

The Companies Act goes further and says a director “reasonably ought” to know important matters in the company. In other words, a director should look beyond what is presented to him and be on the lookout for any other issues that could impact the company.

To gain “reasonably ought” to know information, a director should investigate pertinent matters or may take “other measures” which would result in gaining valuable data – for example, the director may contact an executive director to clarify a matter.

An example to clarify – how to protect yourself from personal liability

- Let’s take “Bill”, a non-executive director of a company which has a subsidiary that imports equipment from China. Bill knows that the subsidiary has purchased a building and owes a R20 million bond on it. The company has guaranteed the R20 million liability.

- Bill has a board meeting in a week’s time and finds that there is no mention of the subsidiary’s bond in his management pack.

- He has read about the new COVID-19 coronavirus and realises that the factory that supplies the equipment to the subsidiary has been temporarily closed and it will take more than a month to get the factory back in production when it reopens. It will then take one month for it to build up stock. Shipping time to South Africa is six weeks. Bill finds out that the subsidiary has only one month’s stock and thus faces potentially about three months of trading without stock. The subsidiary is highly geared, and Bill is concerned that it could stop trading which would mean the R20 million guarantee will be called up and this could affect the company’s solvency.

- Naturally, Bill carefully documents all of this and raises his concerns at the board meeting.

- A majority of the board are reassured by the executive directors that Bill’s concerns are not valid. Four months later, the subsidiary ceases trading, and it and the company end up in liquidation.

- An investigation is carried out and one of its findings is that the company “reasonably ought” to have anticipated that the coronavirus would create solvency problems for the subsidiary and their failure to act has caused both companies substantial losses. Consequently, the directors are personally liable for these losses.

- Not all directors of course, as Bill shows the investigators the work he did and how he was outvoted at the board meeting. He avoids being held liable for the losses.

Directors be wary of this – don’t just rely on management packs etc but also look for the matters you “ought to know” about. This applies also to alternate directors and senior managers who are deemed by the Companies Act to effectively have the powers of directors.

|

|

Your Tax Deadlines for March 2020

|

- 6 March – Monthly PAYE submissions and payments

-

25 March – VAT manual submissions and payments

-

30 March – Excise Duty payments

-

31 March – VAT electronic submissions and payments

-

31 March – CIT Provisional Tax Payments where applicable

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|