|

|

| |

|

May 2017

|

Collecting Arrear Levies: A New Risk for Your Body Corporate

|

“… the difficulty experienced by bodies corporate in collecting arrear levies is not a novel one. It is part of a ‘socio-economic problem’” (extract from judgment below)

Levy collections are the life blood of sectional title schemes, and collecting them is likely to get harder with the economic fallout from our downgrade to junk status.

So if you own property in a scheme, and particularly if you are a trustee of your body corporate, you need to know about the new SCA (Supreme Court of Appeal) decision which puts at risk the body corporate’s right to apply for sequestration of levy defaulters.

Why apply for sequestration?

Applying for the sequestration of a recalcitrant debtor’s estate can be a very powerful debt collection tool. But it should generally only be used as a last resort, and it isn’t always open to you. The facts of the SCA case provide a perfect example –

-

Two sisters jointly owned a sectional title unit, bonded to a bank.

-

When the sisters fell into arrears, the body corporate obtained judgments against them for a total of some R115k.

-

Their movable assets were sold by public auction, but for only R3k.

-

The body corporate then obtained a warrant of execution against the unit and sold it for R170k. The sale however was abandoned when the bank refused to accept the selling price.

-

Having exhausted “all reasonable execution remedies”, the body corporate applied to the High Court for the sequestration of one of the owners. The clear benefit to the body corporate of doing so was that the trustee of the insolvent estate would have sold the unit, and – per the Insolvency Act’s provisions – the arrear levies claim would have been paid as “a cost of realisation” i.e. before the bondholder’s secured claim.

-

Unsurprisingly, the bondholder opposed the sequestration application, arguing that as its bond instalments were up to date, no creditor would benefit from a sequestration other than the body corporate.

-

The High Court refused to order sequestration, and the SCA upheld that decision on appeal.

There must be advantage to creditors as a whole

To understand why the body corporate’s application failed, we turn to the Insolvency Act’s requirement that there must be “reason to believe that it will be to the advantage of creditors of the debtor if his estate is sequestrated”. Bear in mind here that on sequestration what counts is creditors in the plural – as the Court put it “the rights of the creditors as a group are preferred to the rights of the individual creditor.”

In a nutshell, to succeed in sequestrating a debtor’s estate, you need to prove “a tangible benefit to the general body of creditors”. There should be “a reasonable prospect of some pecuniary benefit to the general body of creditors as a whole”, a requirement that will be fulfilled “where it is established that there is reason to believe that there will be advantage to a ‘substantial proportion’ or the majority of the creditors reckoned by value”.

The body corporate failed in this case because it was unable to show pecuniary (monetary) benefit to any creditor other than itself.

Catch-22, and nipping arrears in the bud

“A catch-22 is a paradoxical situation from which an individual cannot escape because of contradictory rules” (Wikipedia)

That leaves bodies corporate in a real “catch-22” situation. You are obliged by law to collect levies, but you risk not being able to do so if you have to rely on what should be your strongest fall-back position - realising the value in the sectional title unit itself.

The bottom line for bodies corporate is this - unless and until our laws are changed to grant bodies corporate immunity from the Insolvency Act’s provisions, you need to prioritise and strengthen your levy monitoring and collection procedures so as to nip any arrear situations in the bud.

|

|

Directors and the “Delinquency” Danger

|

“Directors have clear responsibilities to the public in the form of investors, creditors, shareholders, employees to perform in a fashion wherein not only does the company behave in an accountable manner to these stakeholders but that it adheres to a level of transparency which ensures that the principle of accountability is vindicated” (extract from judgment below)

Directors face many challenges, not least amongst them the constant danger of being held personally liable for any failure to comply with their statutory duties. In addition to facing civil claims for losses sustained, and even possible criminal liability, directors risk being declared “delinquent”.

And that’s no small thing, with serious categories of misconduct risking disqualification from holding any directorship or senior management position for a period ranging from 7 years to a lifetime.

A range of less serious categories of misconduct could result in “probation” - risking disqualification for up to 5 years, supervision by a mentor, remedial education, community service and payment of compensation.

Who can apply for a delinquency order?

Applying for a delinquency order is an effective means of holding directors to account. Thus, most applications are by the affected company itself, its shareholders, its officers, or trade unions/employee representatives. Application can also be made by the Takeover Regulation Panel, certain organs of state and the CIPC (Companies and Intellectual Property Commission).

7 years in the wilderness after an International Airport plan fails

Now, in what could be a sign of things to come, the CIPC has itself taken the bull by the horns and applied successfully for a delinquency order –

-

The CIPC asked for a lifetime delinquency order against a director of a public company which had, it said, bought land for some R140m in order to erect an international airport at a cost of R1bn.

-

The company raised substantial sums of money from public share subscriptions but no Civil Aviation licence to proceed with the planned airport ever eventuated (there was dispute over whether it had even been applied for).

-

Allegations were made that the company continued trading whilst commercially insolvent (at the end it had R600 in its bank account), amounts had been transferred from the company bank account to the director’s bank account, and the company had no proper accounting system.

-

Finding for the CIPC, the Court held that “It was grossly negligent for a director to have allowed a company to continue business in so parlous and insolvent a set of circumstances, to extract company cash in order to pay directors fees and to continue business in the clear knowledge that the Civil Aviation Authority was not prepared to grant permission for the crucial element of [the company]'s business and to allow a public company to operate without proper accounting systems.”

-

The Court declined to grant the lifetime delinquency order asked for, but declared the director delinquent for 7 years. That’s 7 years in the wilderness for him as far as any possibility of company directorship or senior management position is concerned.

Note that although this particular case involved a public company, these provisions apply to all directors of all types of company.

|

|

Landlords v Tenants - Who Pays for Unauthorised Repairs?

|

|

You rent a house and the geyser packs in or the pool starts leaking. The landlord ignores your pleas to fix the problem – or outright refuses to do so. Can you go ahead and do the repairs yourself, then deduct your costs from your rental payments?

A recent High Court case illustrates the dangers of doing so.

The tenant who charged for repairs then short-paid his rent

-

A tenant claimed to have incurred costs in remedying a long list of defects in the rented house, including doors without keys, electrical repairs, pool motor repairs, re-marbeliting of the pool, a gate motor, installation of a geyser, and others. He even billed the landlord for 5 hours of his time spent fixing a water pipe (at “double rate since it was in the midnight hours”).

-

He deducted his charges and costs for these repairs from his rental payments and then, in arrears to the tune of over R200k, defended an eviction application against him on the basis that the landlord had authorised the repairs and deductions.

-

The landlord denied having authorised any repairs, and it didn’t help the tenant’s case that an upfront inspection of the premises (jointly with the landlord’s agent) had failed to reveal any of the defects complained of. In any event his defence was completely destroyed by the specific terms of the signed lease –

- No alterations to the house or its fittings could be made except with the landlord's prior written consent. The tenant was unable to produce any written proof of consent, let alone persuade the Court that he even had verbal consent.

- The tenant couldn’t claim any compensation for any alterations or additions to the premises or its features, whether with the landlord's consent or without it.

- Rental and all other amounts payable had to be paid on time, monthly in advance, “without any deduction or setoff whatsoever”.

- Any changes to those clauses had to be in writing and signed by both parties to be valid.

-

The Court accordingly gave the tenant 30 days to vacate or be evicted by the Sheriff.

So who pays for what?

Landlords have a number of statutory obligations in relation to maintaining the house in good order and repair, but beyond that what counts most is the provisions of the particular lease that you sign.

So before you sign anything make sure you understand exactly what you are letting yourself in for. Pay particular attention to clauses specifying who must do what by way of repairs and upkeep – you will probably be responsible for minor and day-to-day maintenance issues but watch out for those landlords who try to put a much heavier burden on you.

Two final tips

-

Don’t make the mistake that the tenant in this case made of not identifying and recording all defects in the premises in a joint upfront inspection.

-

Both landlords and tenants should take photos of every part of the house before occupation and again after vacation. An app like “Guard My Lease” may help in resolving any later disputes.

|

|

Creditors – Your Special Notarial Bond is Good for 30 Years

|

|

Some good news for creditors here - the SCA (Supreme Court of Appeal) has just held that a 30 year prescription period applies to special notarial bonds.

That’s important because it’s always prudent when making a loan or extending credit to take as much security from the debtor as you can. And whilst a mortgage bond over immovable property is usually going to be first prize here, movables can also provide strong security.

If possible, hold the debtor’s movables yourself and take a pledge over them. Where however your debtor cannot give you actual possession (which is likely to be the case with substantial business assets such as machinery in a factory), consider registering a “special notarial bond” over them.

That will give you the same strong security (in law, not necessarily in practical terms) as you would have with a pledge, even though you don’t have actual possession. Just make sure that each asset is listed in such a way that it is, as required by law for validity, “…specified and described in the bond in a manner which renders it readily recognisable…”, so give full descriptions with any available serial numbers and the like.

What about prescription?

You will know that most debts prescribe after 3 years, but some only after 6 (cheques for example), some after 15 (most State debts), and some after 30 - judgment debts, tax debts, some State debts and “any debt secured by a mortgage bond”.

A creditor’s R500k victory

-

A bank’s loan to a close corporation was secured by a special notarial bond over specified movables. The sole member also signed a personal suretyship.

-

Having failed to pay per the loan agreement, both the close corporation and the member were sued by the bank for just under R500k. They defended the action on the basis that the claim had prescribed after either 3 or 6 years.

-

Agreeing with the High Court that the term “mortgage bond” was wide enough to encompass a special notarial bond, which in consequence won’t prescribe for 30 years, the SCA handed victory to the bank.

If your debtor has significant movable assets, ask your lawyer about registering a special notarial bond over them. Not only will it give you security for your claim, but it will also protect you from a “3 year prescription” defence.

|

|

Your May Website: Money Saving Apps in a Time of Junk

|

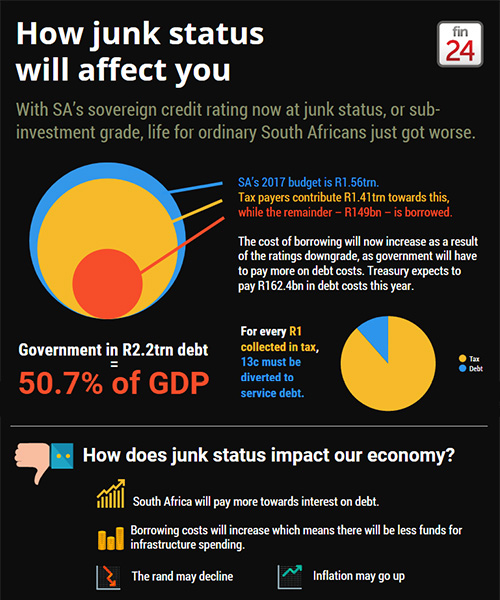

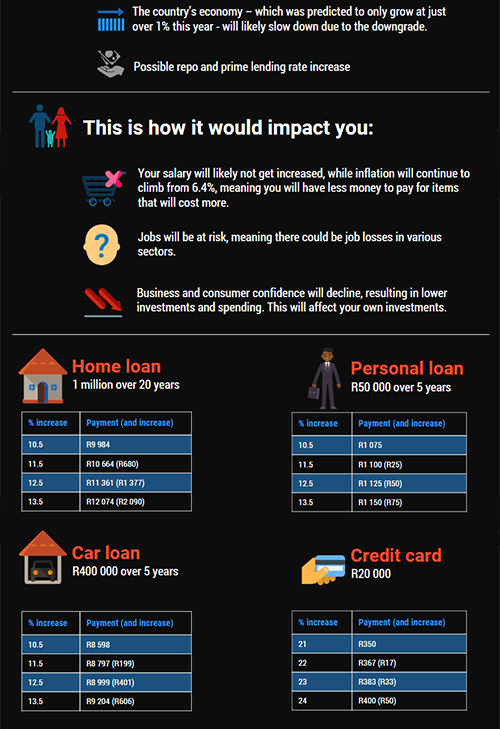

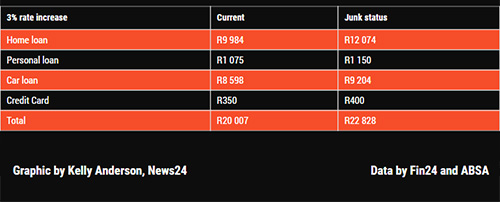

We are clearly in for some challenging times, with predictions of price rises, interest rate increases, and restricted earnings. Fin24’s powerful Infographic “How Junk Status Will Affect You” below says it all -

A good start to surviving until things improve is to control your spending. Have a look at The Citizen’s “Top 5 finance apps you should be using” here.

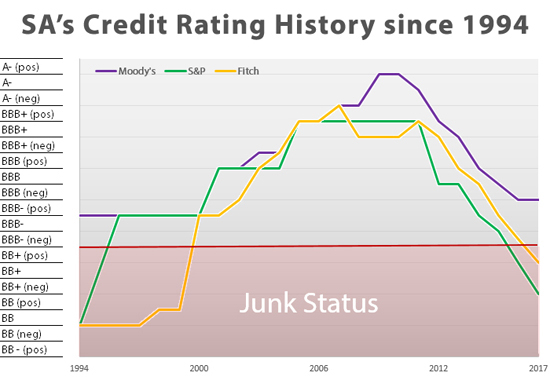

Meanwhile, remember we’ve been here before and we survived it! See this chart of our grading history since 1994 –

Source: Adapted from a Nedbank chart

Also read “Downgrade to junk may not mean disaster – yet” on TimesLive (you may need a subscription) for some interesting thoughts on our first experience of “Junk” since 2000.

“Why ‘junk status’ is not the end of the world for SA” on BusinessTech is another worthwhile read.

Dipping into the OED

“Junk”, n. “Worthless, rubbish”

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|