|

|

| |

|

May 2018

|

Practical Tips on Cash Flow

|

“Never take your eyes off cash flow because it’s the life-blood of business” (Richard Branson)

The Companies Act is underpinned by the assumption of liquidity and solvency – directors and owners are mandated to ensure the business can meet all its short term obligations.

The best way to achieve this is via cash flow.

As cash flow is fundamental to any business, this should be managed by senior management.

The starting point

Sit with your accountant and work out the monthly inflows and outflows from your bank statements. Put them into a spreadsheet and then review this frequently (weekly is desirable) until the cash flows start to get accurate. More importantly you begin to understand the patterns of your company’s cash flows.

Drill down

The most significant aspects of cash flow are:

- Sales. Can I reduce discounts/rebates without losing sales? Is it possible to sell different products to customers? How do I grow my customer base?

Ultimately, no business will flourish without growing sales. Also key to sales is managing debtors:

- How much contact do you have with customers? Getting to know them will reduce the chance of slow payment.

- How quickly do you respond to customer queries? Are credit notes issued promptly?

- Stock. Do you have a good forecasting system to balance not losing sales with minimising stock holding? Is slow moving stock quickly identified?

- Creditors. Do you maximise the possibilities with creditors, for example are all possibilities in terms of early settlement discounts taken advantage of?

- VAT. VAT should be included in your sales figures as well as your purchases, and your VAT return payments factored into your cash flow.

- Work out your free cash flow. This is the excess cash you generate after liabilities have been met. This is crucial to your business as it means you can finance new assets or pay more dividends. Essentially it gives you flexibility and more freedom to grow and run your business.

When you review your business after each month end, build in cash flow to the review. Many businesses now have free cash flow as a key performance indicator.

Cash flow is critical to any business – give it the attention it deserves. It will also give you a good understanding of how the business is performing.

|

|

Here’s what You Should Know About “YES” (our Youth Employment Service) and the Opportunity for SMEs

|

One of the most intractable problems facing South Africa is high unemployment, particularly (and this is a global problem) among the youth. Initiatives to deal with the issue have failed and our unemployment has risen from 21% in 2008 to over 27% at present. Clearly this is not sustainable.

Recently government, business and labour announced the YES (Youth Employment Service) program to tackle youth unemployment. YES will, over the next three years, provide one million young people with a one year’s internship in a business.

The YES initiative recognises that Small and Medium-sized Enterprises (SMEs) are a fundamental driver of employment and seeks their involvement. SMEs should look to get involved as the program is already funded and apart from helping to overcome unemployment, SMEs can reap benefits for their own businesses.

The rationale for YES

Most young people do not get a Matric pass and find it extremely hard to find a job. They thus cannot get the experience and skills to become an effective part of the community. In addition, most of the unemployed youth live in townships which are a substantial distance from businesses.

Currently youth unemployment stands at over 50%.

How YES works

The program has a three-pronged approach:

- In the next three years over 100 companies will sign contracts with 1 million interns. The program will be for at least 1 year and interns will:

- Gain work experience

- Be given practical business training courses (training modules have been developed and will be given to interns)

- Acquire the necessary skills to ensure they will be able to perform in business

- A database of all the CVs of interns will be set up which will be available to companies seeking to employ staff.

- Business hubs will be set up in the townships where training and mentorships will take place. Satellite facilities of SARS, CIPC and B-BBEE accreditators will be available at these hubs. In addition, there will be internet provided along with facilities, including 3D printers, for light manufacturing.

A database will be built up linking township SMEs to the large corporates which will give priority to trading with these small businesses.

- It is unlikely that the 100 larger companies will be able to take on 1 million interns and they will sponsor those who they are unable to accommodate for internships with Black-owned SMEs in townships. This will build up business and employment in these areas.

This is particularly an opportunity for businesses who want to tap into the “Black” market. Why not set up a Black-owned SME in a township and train interns in your products/services and in your business? The interns get knowledge and experience and you can offer employment to the stronger candidates in your business whilst helping other candidates become marketable to other businesses.

Incentives for business to get involved

The interns will earn R3,500 per month. Employers can get this refunded via the Employment Tax Incentive (ETI) which is paid by reducing your monthly PAYE.

There is also the potential to move either one or two places up in your B-BBEE score. A discussion paper is out for comment on amending B-BBEE legislation, the main proposals being -

- In essence companies are set targets as to how many interns they should train and if they exceed their target and offer employment to a percentage of candidates, they move up one position in their scorecard. Companies doubling the number of their target interns and employing double their required quota will move up two positions in their scorecard.

- In addition, companies can claim 50% of their YES skills spend in the Skills Development category.

Remember these are draft proposals and the final legislation could be tweaked.

There will be annual fees (R20,000 for SMEs) for companies who wish to register and participate in the YES program.

Overall, there are plenty of incentives for businesses who wish to participate in the YES program. With most of the large companies putting their support behind this initiative, it will probably be successful and contribute to solving one of the country’s most pressing problems.

|

|

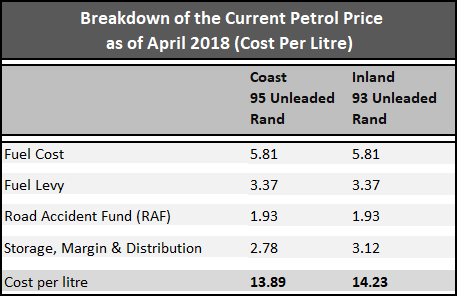

A Tank of Petrol – Where Does Your Money Go?

|

Are you aware that less than 40% of the petrol price is made up of actual petrol cost? Most of it goes to pay tax (Fuel Levy), the Road Accident Fund and the various players in storing, wholesaling and retailing petrol.

As of April the makeup of the cost of petrol (as reported by the Automobile Association) is as shown in the table below.

Notes to the table:

- The difference between the two sets of prices is the cost of transport (34 cents per litre) to get fuel from the coast to inland.

- The Fuel Levy is a general tax and is part of Government taxes. It will contribute R77.5 billion to taxes in 2018/2019.

- The RAF is to compensate those injured in road accidents. RAF will raise R41.2 billion in 2018/2019.

- Storage, margin and distribution is mainly the fee paid to wholesalers and service stations.

|

|

How Big is Your Carbon Footprint and How Can You Reduce It?

|

“We're running the most dangerous experiment in history right now, which is to see how much carbon dioxide the atmosphere... can handle before there is an environmental catastrophe” (Elon Musk)

Climate change is now a part of our life. It is worth getting to know how big our carbon footprint is and how we can reduce it. Of course businesses will also need to start thinking about the new carbon tax planned for 1 January 2019.

Defining “carbon footprint”

It’s the amount of Greenhouse Gases (GHGs) emitted – the main culprits are carbon dioxide, methane, nitrous oxide and fluorinated gases.

The most common ways we emit Greenhouse Gases is by transport, the food we eat, the energy we consume and our shopping spend. If you want to measure your GHGs have a look at The Nature Conservancy’s Carbon Footprint Calculator here.

What should you do to reduce your footprint?

Transportation is now the biggest emitter of GHGs, so it’s a good place to start.

An overseas flight puts 2.6 tons of GHGs into the atmosphere. Do you really need to make that overseas trip when a lot of business can be done on electronic media?

Motor cars come next – if the average person did not use their car for a year it would also save 2.6 tons of GHGs. Consider the following:

- When buying a car consider buying an electric or hybrid vehicle. Generally, the less emissions, the lower your operating costs.

- Minimise the use of your car – use carpools, share a taxi or Uber, or where possible ride a bicycle or walk.

- Service your car regularly and check tyre pressure often.

- To optimise your fuel usage, drive more efficiently by braking less and reducing the amount of air-conditioning you use.

In terms of your home, look at going off grid and converting to renewable energy. If this is too expensive you can:

- Regulate the hours your geyser operates,

- Reduce your meat and dairy consumption,

- Buy a laptop as they use 80% less power than desktops,

- Recycle bottles, packaging etc.

There are many ways to save here, so look at your home and circumstances and analyse how you can cut GHGs.

We have already touched on shopping but reducing what you buy to cut down on waste is a good start. Look at the type of packaging on your purchases – is there wastage by the supplier and how environmentally friendly is it? If we do this correctly we can:

- Save money

- Lead a healthier lifestyle, and

- Reduce CHGs.

Climate change is with us, so let’s approach it in a realistic and responsible way. Let’s also measure how we contribute to CHGs and how we can try to reduce our impact on the environment.

|

|

Bitcoin is Taxable!

|

SARS has released a media statement on Bitcoin in which it states that people dealing in Bitcoins or other cryptocurrencies are subject to normal Income Tax law in terms of gross income, tax deductions or Capital Gains Tax. SARS are treating Bitcoin not as a currency but as an intangible asset.

If you are in doubt about your circumstances speak with your accountant, and in need you can get a ruling from SARS.

Taxpayers who fail to declare dealings in cryptocurrencies will be subject to interest and penalties.

Currently, you are not required to register for VAT if you are a vendor in Bitcoin (or any other internet currency).

|

|

Your Tax Deadlines for May

|

Your annual EMP501 reconciliation for the period 1 March 2017 – 28 February 2018 is due for submission by 31 May 2018, together with all Employees Income Tax Certificates [IRP5/IT3(a)s].

You can submit online via eFiling if you have less than 50 employees, or via e@syFile™ Employer (check that you have the latest version).

It’s important to get this right as penalties will be levied for late submission or inaccurate information, so ask for help in any doubt.

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|