Prepare Now For Leasing Changes That Will Impact Your Business

If your accountant uses IFRS (“International Financial Reporting Standards”) in compiling your financial statements, and if you lease assets, then changes are coming that you need to start preparing for. The International Accounting Standards Board has mandated new accounting treatment from 1 January 2019.

Many businesses have cash flow issues, and as leasing conserves cash, they are users of leasing services. For these businesses, it is worth getting to grips with these new rules.

The good news is there is plenty of time to prepare for the change but the changes will be complex and could have an effect on your ability to get loan finance.

How does it affect me?

With a few exceptions (see below), operating leases will fall away. Instead of writing off lease payments to the income statement, you will be required to bring the value of the leased asset onto your balance sheet and provide for the lease repayments as a liability. Depending on the amount of leases you have, this could materially impact on your balance sheet.

The income statement will also reflect changes. Operating lease costs will now be shown as interest expense and depreciation.

The major changes

The major changes will be:

- All leases will need to be reviewed and unless they fall within the limited exemption rules will need to be capitalised.

- Exemptions include leases of 12 months or less or minor items (see example below).

- Leases for intellectual property, licensing agreements, leases for nongenerative resources (oil, minerals), service agreements and leases for biological assets are also exempt.

- Exemptions include leases of 12 months or less or minor items (see example below).

- You will be required to identify and strip out non-lease components e.g. a photocopier lease contains a service agreement of, say, R150 per month. This R150 per month will be shown separately in the income statement (see example)

- All contracts are to be scrutinised to see if they contain a “right of use”. If they do they will probably fall into the new rules.

- Your asset base increases as the value of the lease is shown as an asset on your balance sheet.

- You show more debt on your balance sheet as the liability for the lease will be included in the balance sheet.

- Overall the changes net out over time but generally expenses will increase in the first few years and then decline in future years.

- Operating profit increases but depreciation and interest expense rise.

- Your cash flows are unchanged.

- Key business ratios change such as Earnings per Share, Return on Equity and the gearing of the business (debt to equity ratio). This could affect how banks view the strength of your balance sheet.

- It can also have internal implications for example if staff bonuses are calculated using say, ROE, their bonus will alter.

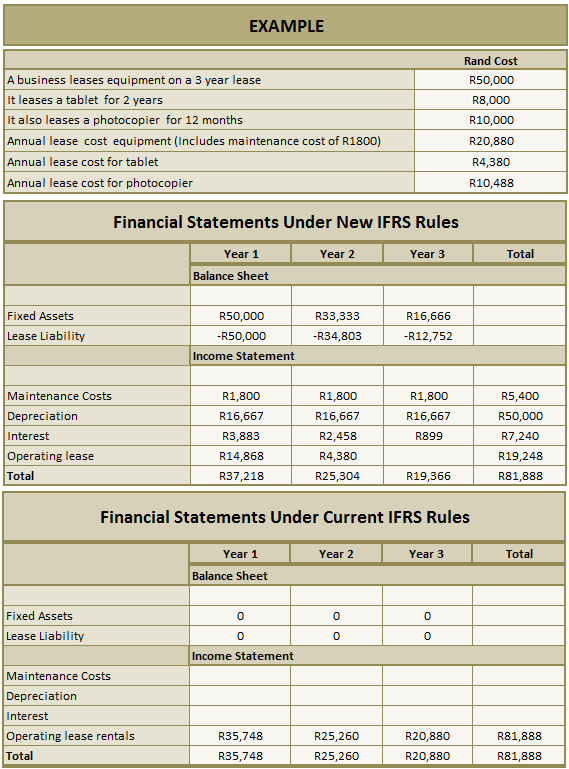

Have a look at this example

An example best illustrates the changes to your financial statements –

NOTES

Start planning now

Depending on the number of leases and contracts you have this could be a time consuming and complex process – especially as you will have to set up new systems, accounting policies and methods of valuing leases. Also you need time to assess the effect this could have on your ability to borrow funds.

Speak to your accountant who can guide you through this process.

|

(If the tables above do not display correctly, please see the “online version” – link above the compliments slip)

- The balance sheet will show a fixed asset for the equipment and a liability for lease owings under the new IFRS rules.

- The differences in the Income Statements net out but note the increased expense shown in year 1 and 2.

- There is no change to lease treatment for small items (tablet) and leases of 12 months or less (photocopier).

- Maintenance costs are stripped from the lease and shown separately under the new rules.

- Cash flows do not change under either scenario.

- Lease cost calculated at an interest and discount rate of 9%.

Start planning now

Depending on the number of leases and contracts you have this could be a time consuming and complex process – especially as you will have to set up new systems, accounting policies and methods of valuing leases. Also you need time to assess the effect this could have on your ability to borrow funds.

Speak to your accountant who can guide you through this process.

Provided by May and Company

© DotNews. All Rights Reserved.