You and Budget 2016

How am I affected? The highlights

(Note that these are proposals, subject to final legislation. The effect on revenue collections is shown in brackets)

- The good news was income tax and VAT rates were not increased. Income tax relief was restricted to lower earners (+R7.6 billion)

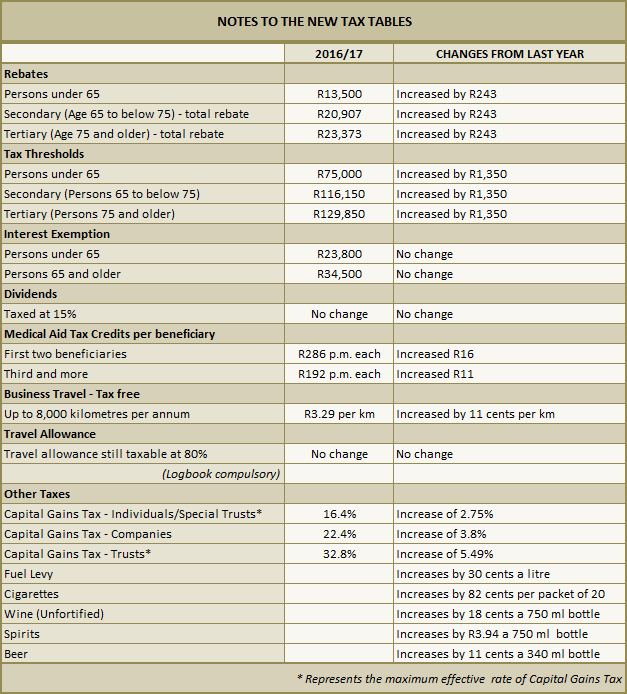

- Capital Gains Tax inclusion rates were increased for both individuals (from 33% to 40%) and companies (from 66% to 80%) – see the table below for the effective rates (what you will actually pay) (+R2 billion)

- Sin taxes (alcohol, cigarettes) were raised (+R2.2 billion)

- Fuel levy up 30 cents a litre (+R6.8 billion)

- Green and health taxes: A new levy on new and retread tyres from October 2016, plus increased levies on plastic bags, light bulbs and motor vehicle emissions, with a new “sugar tax” (only due 2017) aimed at reducing sugar consumption (+R0.5 billion)

- Transfer duty is up for top-end property sales with the introduction of a new band of 13% on sales over R10m (see the table below for details) (+R100 million)

- Increased medical aid tax credits (see the table below) (-R1 billion)

- A new Special Voluntary Disclosure Programme (VDP) will be introduced in October for individuals and companies (but note trusts will be excluded, unless agreed that persons other than the trust effectively hold the assets) to declare undisclosed off-shore assets

- Amendments to retirement taxation have been standardised so that individuals can claim 27.5% of taxable income (up to a limit of R350,000) on pension funds, retirement annuities and provident funds. Employers may continue to contribute to the employee’s retirement funds but this will be taxed as a fringe benefit to the employee and will be part of the R350,000 allowable deduction

- Trusts: Also proposed (it has to go through the usual approval process and the final legislation may well differ from the proposal) is that assets will, if transferred to a trust via loan account, fall into the founder’s deceased estate, and that interest free loans to trusts will be treated as donations.

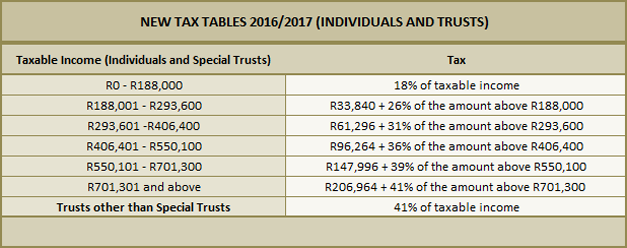

The new tax and transfer duty tables

(If the tables above do not display correctly, please see the “online version” – link above the compliments slip)

Provided by May and Company

© DotNews. All Rights Reserved.