|

|

| |

|

JANUARY 2016

|

Starting a business in 2016? 3 steps to get you going

|

“In the middle of difficulty lies opportunity" (Albert Einstein)

It seems as though 2016 has a rough ride in store for us but as the wise old saying has it: “Fortune favours the brave”. Just remember to mix a good dose of realism in with the bravery.

That said, if you’ve been sitting on a brilliant business idea, and if you’ve ever dreamt of leaving your 9 to 5 job and starting up on your own, this could well be your year!

Get going with these 3 steps -

- Consider checking first that you are suited to the excitement, rewards, risk and rough-and-tumble of entrepreneurship by taking the “Entrepreneurial Personality Profile” test on the Psychology Today website at http://psychologytoday.tests.psychtests.com/take_test.php?idRegTest=3204.

- Passed the test? Great, next step is to get off on the right foot with “Starting a business: Ten simple rules for a successful start-up” on the Business Partners website athttp://www.businesspartners.co.za/starting-a-business/. (Tip: Don’t ever lose sight of Rule 10 “Enjoy Yourself"!)

- All done? Stage 3 is to choose the right trading vehicle to suit your particular needs and those of your new business. This is important – starting off with one legal entity and then later moving the business to another type risks all sorts of unhappy legal and tax issues (quite apart from all the obvious practical ones, like wading through piles of red tape at SARS, Telkom and your bank’s “please hold, your call is important to us” call centre).

Choose the right legal entity!

In South Africa you have these four main options to choose from –

- A sole proprietorship (“sole trader”). Only one owner – you are the business.

- A partnership of 2 to 20 owners.

- A private company (“Pty Ltd”) for any number of owners (“shareholders”). Note that CCs (close corporations) still exist, but no new ones are registered.

- A business trust (also any number of owners).

There are other specialised types of company available only to non-profit organisations (charities and the like), and to professionals (lawyers, accountants, doctors etc) and various ways in which different legal entities can be combined, but to start with let’s stick with the four basic options above.

In future articles we’ll look in detail at each of these four options but, and this is vital, don’t make any decisions without first seeking professional advice on the legal and tax implications of using each type of entity. There are a lot of minefields here!

This is the first article in our series “Choosing the right legal entity for your business”. Next time we’ll look in more depth at the “sole proprietorship” option.

|

|

Property sellers: just how far does your duty to disclose go?

|

“Where a seller recklessly tells half-truths or knows the facts, but does not reveal them because he or she has not bothered to consider the significance, this may also amount to fraud” (extract from judgment below)

Firstly, a note on the CPA

What is said below does not pertain to those property sales where the very robust buyer protections in the CPA (Consumer Protection Act) apply. Generally speaking the CPA applies only where the seller is selling “in the ordinary course of business” (a developer for example), and most private sales will fall outside its ambit. That whole question is however a big topic on its own so watch this space for a future article on “Voetstoots v CPA”.

Voetstoots – the limits

You will know how vital it is for property sellers to protect themselves with a correctly-worded “voetstoots” clause in the sale agreement. It effectively provides that the property is sold “as is”, so the buyer carries the risk of there being any “latent” defects (i.e. those “not visible or discoverable upon an inspection”), and the seller is only responsible for them if the buyer is able to prove that the seller –

- Knew of the latent defect at the time of the sale, and

- Did not disclose it, and

- Deliberately concealed it with the intention to defraud.

In other words as a seller, if you know of a defect you must disclose it to the buyer. Record any disclosure/s in a written and signed annexure to the deed of sale.

In real life of course there are often grey areas around what exactly is or is not “a defect” and when you will or will not be taken to have acted fraudulently in not disclosing it.

But as a recent High Court case illustrates, it is probably best to err on the side of caution here -

A most unlevel house

- The foundational wooden structures of a timber house had decayed, causing the house to subside on one side, with the result that the floors were no longer level.

- To remedy this, the owners had put a cement screed over the wooden floors and covered them with carpeting. So too the ceilings were levelled by means of a false ceiling.

- The subsequent buyers only found out about these problems when they tried to effect renovations. They sued for cancellation of the sale, damages and/or a reduction in the purchase price.

- The sellers, relying on a voetstoots clause, denied all knowledge of the decayed foundations, denied that the unlevel floors and ceilings were “defects”, and claimed to have remedied them purely for aesthetic reasons and without intending to conceal anything.

- Finding for the buyers, the Court noted that a “defect” is “any material imperfection preventing or hindering the ordinary or common use of the [property]”, and held that the unlevel floors and ceilings were clearly latent defects – the buyers would not have bought the house had they known of them.

- Moreover, the sellers should have disclosed these defects because, although they “never considered the significance” of doing so, our law is that: “Where a seller recklessly tells half-truths or knows the facts, but does not reveal them because he or she has not bothered to consider the significance, this may also amount to fraud”.

- In any event, said the Court, a seller has a duty to disclose any “unusual or abnormal qualities” in a house, and the uneven floors were such an unusual feature that they should have been revealed.

Buyers – be warned

Be warned that depriving a seller of the protection of a voetstoots clause is never going to be easy, particularly since you will need to prove that the seller intended to defraud you by concealing a defect. Rather be sure of the condition of the house and property before you buy – consider for example using a trustworthy home inspection service to check everything out for you.

|

|

The Case Of The Electrocuted Cyclist - More Risk For Suppliers

|

If you operate anywhere in a product supply chain (producer, importer, distributor, retailer, supplier, installer etc) be aware that your risk of being sued under the CPA (Consumer Protection Act) just increased.

First “No Fault”, now even wider liability

To recap, the CPA makes you liable for any form or level of damage to person or property resulting from defective or unsafe products.

Critically, there is no need to prove any form of negligence on your part – liability is now “no-fault” or “strict”. And whilst there are a few defences still open to you, they are limited.

Now a new and important High Court judgment has established that your liability is not limited to the “consumer” of the product; you are liable also to “innocent bystanders” and the like. That’s a lot more risk.

On fire: An electrocuted cyclist sues Eskom

- A cyclist had the misfortune to ride into a low-hanging live power line spanning a footpath.

- Electrocuted so severely that his clothes caught fire, he was saved only by the quick thinking and actions of his companions, who were fortunately able to pull him free, extinguish the flames, and resuscitate him after he stopped breathing.

- Severely injured, the cyclist sued Eskom for substantial damages under the CPA.

Are you liable only to “consumers” or to everyone?

- Eskom admitted that it was responsible for the power line and that it was both the producer and distributor of the electricity. But it denied liability, relying on the fact that the cyclist was not in this case acting as a consumer or user of electricity, and arguing that the CPA protects only “consumers” of products, and no one else.

- The Court however, having analysed the wording, spirit and purpose of the CPA, disagreed. It held that you need not be a “consumer in the contractual sense” to have a claim. A third party such as an innocent bystander would also be covered. The cyclist is therefore entitled to recover his proved damages from Eskom.

Manage your risk

- Take legal advice on the extent of your exposure, have all your supply contracts, usage instructions and warnings checked, and beef up your quality control procedures.

- Check that your product liability insurance covers you for CPA strict liability claims to innocent third parties as well as to consumers.

|

|

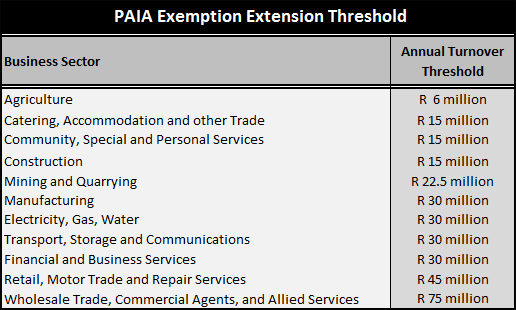

Paia Manuals: Another Last Minute Extension

|

“Procrastination is the thief of time” (Edward Young, 18th c. poet)

If your business is one of those (mostly smaller – see below) businesses temporarily exempted from lodging your PAIA manual until 31 December 2015, you will be happy to hear that the pressure is off for another 5 years, and that the turnover thresholds have been increased. This is now three times since 2005 that government has, after telling us there will be no further extensions, done an about-face at the very last minute.

Don’t kick yourself however if you rushed to beat the deadline - you will almost certainly still have to comply somewhere down the line, and at least you crossed off one annoying little red tape item from your To-Do list.

Procrastinators on the other hand are doomed to repeat the eleventh-hour panic in 2020. Rather comply now if you haven’t already done so.

Does this extension apply to you?

The new 31 December 2020 deadline applies to most smaller businesses - specifically to any “private body”, including any private company, but not to any non-private company, nor to any private company in any of the business sectors listed below with either -

- 50 or more employees, or

- An annual turnover of or above specific thresholds – see the table below for details.

(If the table above does not display correctly, please see the “online version” – link above the compliments slip)

|

|

|

Your January Website: How To Turn New Year Resolutions Into New Year Realisations

|

We all know just how hard it is to keep those New Year’s resolutions. The year kicks in, it’s back to work, routine takes over…..

Don’t let that happen this year. For some great ideas on actually realising your resolutions read “44 Ways to Kick-Start Your New Year” on the Success Magazine website at http://www.success.com/article/44-ways-to-kick-start-your-new-year.

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|