|

|

| |

|

July 2017

|

Tax Season Opened On 1 July: Here’s What You Need to Know, and Do

|

“Giving money and power to government is like giving whiskey and car keys to teenage boys” (P.J. O'Rourke)

Once again tax season has opened for individuals, and whilst we can chuckle at jokes about the pain of paying taxes, they remain of course an integral part of life.

By now you should have already gathered all your supporting documentation. This is an important task as not getting your tax 100% correct can lead to queries and audits from SARS, which is clearly something to avoid. Whilst you won’t have to submit this with your tax return, you need to keep it available, for five years, in case SARS asks for it. Once an audit is open or if you must prove the item you need to retain documents for longer.

However, if you are going to do your return at a SARS branch, then bring all your documentation and your I.D. with you.

Documentation you will need is …

- Your IRP5. If you changed jobs during the year, you will have at least one other IRP 5. If you get any retirement funding, the relevant institution will send you an IRP 3 (a).

- IRP 3 (b) for any investment income received.

- Medical certificates from your medical aid plus any medical expenses incurred not covered by medical aid.

- A logbook if you receive a car allowance.

- Any retirement funding certificates received.

- Any other documentation that will affect your return e.g. if you had a capital gain or loss during the tax year.

Check that the tax certificates you receive are correct and if you find an error, go back to whoever sent you the documentation and get them to issue a corrected certificate. SARS populate your tax return with information received from third parties (IRP5, IRP 3 etc) and the only way to change the populated data on your tax return is to get the tax certificates re-issued. This can be a very cumbersome process.

Do you have to submit a tax return?

If you earn R350,000 or less -

- From a single employer,

- You have no other tax deductions, such as a car allowance or retirement funding,

- You earn less than R23,800 in interest from South Africa (if you are less than 65 years old) or R34,500 in interest (if you are 65 or over),

- You are a non-resident with only exempt dividend income.

Then you are one of the lucky people who don’t need to complete a tax return. There are a couple of exceptions here, so if in doubt speak to your accountant. If you submit a return where you were not required to, this may, due to the SARS systems, lead to an automatic imposition of penalties and this may in turn lead to unnecessary disputes with SARS.

Of course if you are due a refund, then you should submit a tax return anyway.

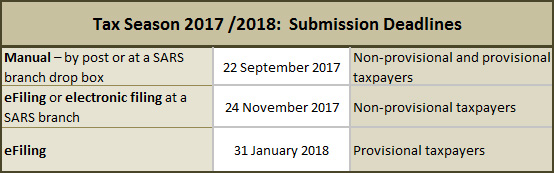

Submission deadlines

Important dates to file your tax returns for the 2016/2017 tax year are as per the table below.

Be honest when compiling your return. Check that everything is correct and accurate. Finally, be alert to the scammers out there who always seem to target SARS related transactions.

|

|

Vet Your Suppliers! Good Stakeholder Relationships Will Boost Your Profits

|

Suppliers play a strategic role in your business because if they fail to deliver on time or with the required quality, they can cause delays in your organisation. These delays will inevitably have a knock-on effect to your customers.

How to ensure you get high quality suppliers

Best practice dictates that vetting procedures are in place that cover, at least:

- A review of the supplier’s financials to establish that the business has the financial means to remain sustainable and to deliver to its customers.

- The supplier has sound processes in place and the organisation is well managed.

- How long has the entity been in business? The longer the better.

- Get testimonials from the supplier’s current customers.

- Check for fraud and/or conflicts of interest. This involves establishing that none of your staff have undisclosed relationships with the supplier, that the supplier has no criminal record or any suspicious activities.

- See how the supplier responds to queries. You could call as “customer” of the supplier and see how they react to a problem.

- Check their social media platforms to ensure they are consistent with their marketplace persona.

- Culturally are they a good fit for your business? Do they have the same values as your organisation?

- Have in place ongoing processes to detect if there are any changes in the supplier’s organisation which could trigger further investigation.

Getting the most out of suppliers

In the new King IV Report there is a section on optimising stakeholder relationships by an “inclusive approach that balances the needs, interests and expectations of material stakeholders in the best interests of the organisation over time”.

This involves understanding what they want and ensuring there is a mutual relationship of trust which will last a long time and from which both parties will get the outcomes they want.

An honest, transparent relationship with your suppliers will bring good long term profit to your business.

|

|

Directors and Shareholders: There’s Hope If You Forget Companies Act Compliance Requirements

|

The “new” Companies Act is pitted with clauses requiring that special resolutions be passed. There are also instances where as directors you are required to take certain actions such as recusing yourself if there is a conflict of interest.

It is important to note that transactions can be set aside if the necessary steps are not taken. Should this happen, a costly and time-consuming exercise would follow.

Can “unanimous consent” rectify non-compliance?

Both our “old” Companies Act and English company law allowed the concept of “unanimous consent” to override statutory non-compliance with certain requirements, such as the requirement for a special resolution to be passed authorising the sale of all (or the greater part) of a company’s assets. Simply put, if all of the shareholders were aware of the implications of a transaction and consented to the transaction, then the “unanimous consent” principle may be available to hold up the transaction despite the required statutory steps not having been taken.

In South Africa following the introduction of the “new” Companies Act in 2011, there was uncertainty whether “unanimous consent” would be accepted here until the Supreme Court of Appeal (SCA) recently pronounced on the subject.

What the SCA said

A company sold the major part of its assets and the directors had a conflict of interest in the sale. Part of the case revolved around setting aside the transaction as no special resolution was passed for the sale of the assets and the directors had not disclosed their interests. The company was owned by a single shareholder – a trust effectively controlled by one person.

The SCA said that the reason for requiring that a special resolution be passed was to “ensure that the interests and views of all shareholders are taken into account”. When reviewing the circumstances of this case the SCA found that the person who controlled the sole shareholder was party to the transaction and thus no special resolution was needed as the shareholder was clearly aware of and had effectively approved the transaction.

It used a similar line of reasoning in resolving the conflict of interest question.

The court specifically accepted the principle of unanimous consent, stating “that principle, long recognised in English company law, from which our courts have received much guidance, was accepted as part of our law relating to companies, under both the 1926 and the 1973 Companies Acts. I can see nothing in the current Act to suggest that the principle no longer finds application”.

The implications are that if a business is owner-managed or the board of directors are a tightly knit group then – even if in error you don’t tie up all the Company law requirements - the “unanimous consent” principle might be available to you.

Be sure however to seek professional advice – every situation will be different.

|

|

Must You Pay Tax on Bitcoin Transactions?

|

Bitcoin has become increasingly used in South Africa and there are some good platforms for its use. Although it has proved volatile (it fell 30% in value recently), its long term value has risen over the past decade.

So is Bitcoin subject to taxation? Yes it is. South Africa is following global trends and SARS has confirmed that the normal rules of taxation will apply and it will be subject to income tax or capital gains depending on the type of transaction.

Speak to your accountant if you need advice.

|

|

Blockchain Technology: New Potential in Financial Services

|

Bitcoin is currently the best known user of a blockchain platform, but expect many more varied uses to emerge.

For example Calastone, which provides a platform for mutual funds (e.g. unit trusts) to trade in 34 countries, recently successfully replicated its transactions for a full day using blockchain technology.

Will this be good for us?

This potentially paves the way to transform the industry, resulting in enhanced and faster access to global and local securities at a significantly lower cost.

The financial services industry has been in a race to be the first to use blockchain technology.

|

|

In The News Again: Mandatory Audit Firm Rotation

|

The Independent Regulatory Board for Auditors (IRBA) has proceeded with its aim of introducing Mandatory Audit Firm Rotation (MAFR), which will apply only to listed companies and public interest entities (institutions such as banks and insurers) and is intended to “enhance auditor independence and protect public interest”.

Recently the head of the IRBA and the Finance Minister announced that this would commence on 1 April 2023.

There has been a backlash to this by prominent bodies such as the King Committee, the Institute of Directors and the Chief Financial Officers Forum (Finance Directors of JSE listed companies). The opposition centres around the cost of the move to MAFR, estimated at R10 billion in the first ten years and whether the intended purpose of MAFR will in fact be achieved. A number of countries who previously introduced mandatory rotation have in the meantime scrapped this for the same reasons.

MAFR, say those opposed to it, will effectively dilute shareholder rights and will lead to less investment in South Africa, as it will deter companies from listing on the JSE.

These bodies have appealed to Treasury to reconsider the matter. These are strong words and we will update you as this unfolds.

|

|

Your Tax Deadlines for July

|

There are no significant tax reporting deadlines in July.

However, tax season is one of the most significant events in the tax calendar. As noted above, it opened on 1 July, and you need to know whether or not you are required to submit a return, and if so, what documentation you need and what deadlines you must meet.

|

|

Note: Copyright in this publication and its contents vests in DotNews - see copyright notice below.

|

| |

|

|

|

|